How to Budget As a Couple for a Happier Wallet

If you and your partner can agree on where the money goes, you can actually enjoy the ride together instead of pretending you’re battling a spreadsheet dragon. Let’s cut to the chase: budgeting as a couple isn’t about restriction; it’s about freedom—freedom to plan, to save, to live. And yes, you can do it without losing your sanity or your Netflix password.

Kickoff: Decide on your money vibes

Budgeting works best when you’re on the same page. Start by answering a couple of simple questions together: What do we actually want? What scares us about money? Do we save like squirrels or splurge like it’s a Friday every day? IMO, you don’t have to have all the answers right away, but you do have to talk about them honestly.

– Share your money goals for the next 6–12 months.

– Talk about non-negotiables (rent, student loans, essentials) versus nice-to-haves (date nights, solo hobbies).

– Agree on a workflow you’ll actually follow. Weekly check-ins beat monthly marathons.

Lay the foundation: track, then plan

If you don’t know where the money goes, you’ll keep guessing and probably arguing about coffees you didn’t need. Start with a clean slate: track your income and all expenditures for a month. FYI, you’ll be surprised how often tiny costs add up.

- List every income source (salary, side gigs, whatever).

- Record every expense, big and small (groceries, vending machine sins, your share of rent).

- Categorize into needs vs wants. If you’re honest, you’ll see gaps and overlaps.

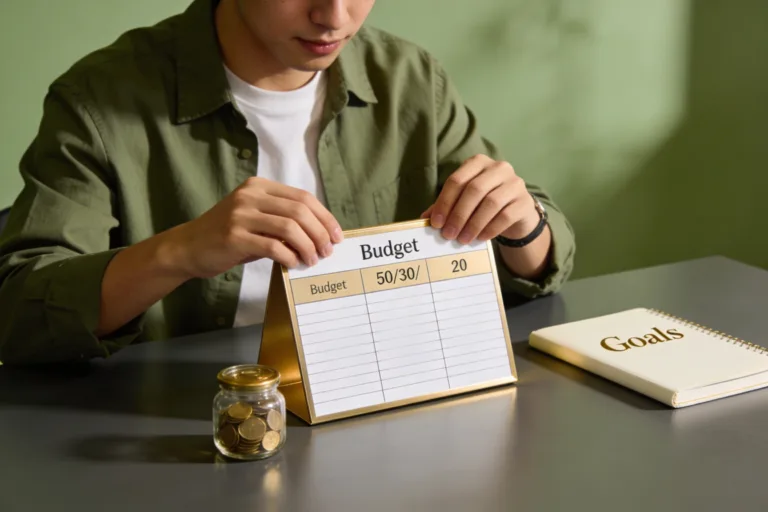

Smart budgeting templates you can steal

– 50/30/20, but make it couple-friendly: 50% needs, 30% wants, 20% savings or debt payoff.

– 60/20/20 when you’ve got big goals: 60% needs, 20% savings, 20% leftovers for splurges.

– Envelope-style for discretionary spend: cash for date nights, groceries, and fun money.

Pick a system you’ll actually use

There’s no holy grail of budgeting. There’s only what sticks. Do you both hate apps or live for spreadsheets? Pick a system and commit to it for 90 days. Then reassess.

– Shared app or spreadsheet? Pick one place for all money talk.

– Pillow talk budget: set a weekly budget talk date. If life gets wild, you’ve got a built-in reminder.

– Separate accounts, joint goals: keep independence but align on core goals.

Two common setups

– The joint bucket with personal slush funds: one savings pot for shared goals, plus a small personal fund for each person’s own treats.

– Fully merged, fully transparent: every penny belongs to the couple. Sounds intense, but it builds trust and can simplify decisions.

Deal with debt and big goals like adults

Debt can whisper “you’ll never get ahead” in your ear. Don’t listen. Create a plan you both own, and attack it together.

- Identify the highest-interest debt first. Snowball or avalanche—pick the method that keeps you motivated.

- Set a realistic payoff timeline. If you say “never,” you’ll start arguing in month six.

- Automate payments. If you forget, automation remembers for you.

When you’ve got different debt feelings

If one of you is a thrill-seeking spender and the other is a debt-averse saver, agree on a compromise: a small, controlled discretionary fund for the spender, with a hard ceiling to prevent binge debt. FYI, balance is your friend, not your prison warden.

Make room for life: fun, date nights, and spontaneity

Budgeting doesn’t mean “no fun” forever. It means “fun, within reason.” You’ll actually have more fun when you’re not stressing about money all the time.

– Create a date-night fund: a small, fixed amount each month pays for joy without guilt.

– Plan micro-delights: a coffee, a walk, a movie night at home—costs less, feels bigger.

– Keep a “kid in a candy store” moment fund for spontaneous adventures—without sabotaging goals.

How to say yes to the fun without wrecking the plan

Use a “cap and capper” rule: a monthly cap for discretionary spending, plus a buffer. If you hit the cap early, you cool it for a bit or switch to cheaper options. Simple, fair, and prevents resentment.

Communication tips that actually work

Money talks can derail even the strongest couple. Here are tactics that help you stay aligned instead of arguing in the grocery store aisle.

– Schedule regular check-ins, not emergency meetings. Consistency beats chaos.

– Avoid blame language. Say “I feel” rather than “You spent.”

– Celebrate wins. Small milestones deserve big kudos.

– Use “we” language. You’re a team, not two players on opposite sides.

Conflict-proof phrases you can steal

– “Let’s pause and revisit this tomorrow.”

– “What’s the real priority here?”

– “If we both put this amount here, what changes next month?”

Emergency fund and safety nets

Life loves to surprise you with late fees, car trouble, or a surprise vet bill. Prepare for it now so you don’t crash later.

– Target: 3–6 months of essential expenses in an easily accessible account.

– Automate small monthly deposits until you hit the target.

– Keep a separate cushion for irregular expenses (car maintenance, annual insurance, holidays).

Where most couples go wrong

They dip into the emergency fund for non-essentials. Don’t do that. Treat it like a medical emergency: only for actual emergencies.

FAQ

How do we handle income inequality in a relationship?

Talk openly about how each income stream affects your budget and goals. Decide whether to pool everything or keep some separate. The key is transparency and fairness—no secret bonuses or hidden “extras.” If one person earns significantly more, consider a tiered approach: shared essentials funded from a common pot, with personal discretionary funds that feel like “mine.”

Should we split everything 50/50?

Not necessarily. Split based on ability to contribute and your goals. If one partner earns less but contributes in other ways (home management, heavy lifting with chores, emotional support), you can adjust. The important thing is that the plan feels fair to both of you.

What if we disagree about spending?

Use a structured process: a weekly check-in with a single decision-maker for that week, or a mini vote. If you still disagree, default to the budget line item and table the debate for 24 hours. FYI, time and a good night’s sleep can work wonders.

How can we save more without killing our fun?

Automate savings and set realistic targets. Combine with small rewards when you hit milestones. Think of savings as a monthly date with your future self—yes, you deserve it, and yes, you’ll thank yourself later.

Is it okay to keep separate accounts?

Yes, if it helps you stay sane. Shared goals stay in a joint account, while each person can have their own fund for personal treats. The compromise: clear rules on what counts as shared vs. personal contributions.

Conclusion

Budgeting as a couple isn’t a boring chore; it’s a shared game with clear rules and a victory lap at the end. When you’re both in, you’ll reduce drama, boost trust, and actually enjoy planning your future together. Start simple, keep it human, and tweak as you learn what works. You’ve got this—and FYI, the best financial decisions you’ll make this year are the ones you make together.