Simple Budget Planners That Actually Work 💸

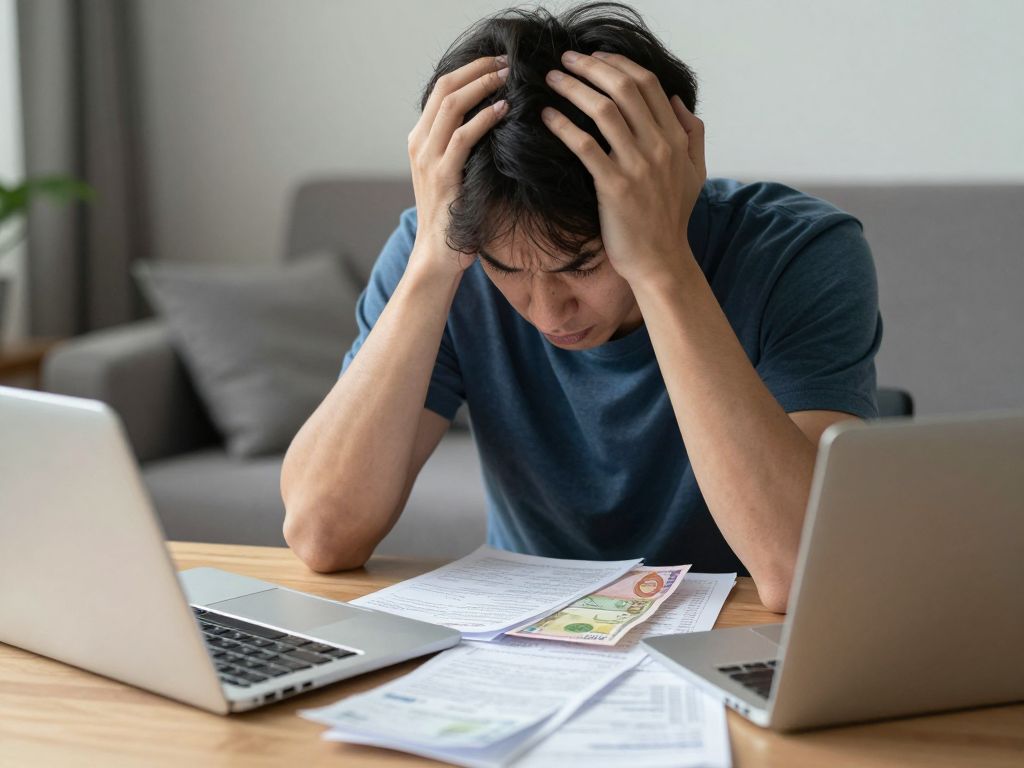

I used to swear I “wasn’t a budget person.” Then my checking account overdrafted over a $7 iced latte, and my pride evaporated faster than that coffee. Ouch. That moment pushed me to try simple budget planners instead of fancy apps that felt like NASA dashboards. Guess what? They worked.

I realized quickly that most money stress doesn’t come from how much you earn, but from how little you track. When I started writing things down in a basic planner, my anxiety dropped, my savings grew, and my money finally made sense. Ever had that feeling where your bank balance looks like a mystery novel with a plot twist you didn’t sign up for? Yeah, me too.

If you want control without complexity, simple budget planners can change your life. You don’t need spreadsheets with 47 tabs or AI predictions about your avocado toast habits. You just need a clear system you’ll actually stick with. Ready to talk about what really works? Let’s go. 📒

Why simple budget planners beat fancy apps

Apps look shiny, but shiny doesn’t mean effective. I’ve downloaded at least six budgeting apps, used them for two weeks, and ghosted them like a bad date. Meanwhile, my paper planner stayed loyal.

Simple budget planners work because they reduce friction. You don’t need Wi-Fi, passwords, or notifications yelling at you like your mom. You just open the page and write.

They also force mindfulness. When you physically write “$120 — groceries,” your brain pays attention. Ever notice how tapping numbers on a screen feels way less real?

Here’s what simplicity gives you:

- Clarity instead of chaos

- Consistency instead of overwhelm

- Control instead of confusion

- Confidence instead of panic

IMO, that’s a solid trade-off. 🙂

What makes a planner “actually work”

Not every cute planner deserves your money. Trust me, I’ve bought pretty ones that looked Instagram-ready but functioned terribly. So what separates winners from dust collectors?

Clear layout beats aesthetic

A planner must show your money story at a glance. You should see income, bills, spending, and savings without squinting.

Look for these must-haves:

- Monthly overview page

- Bill tracker

- Spending log

- Savings tracker

- Debt payoff section

If you need a decoder ring to understand it, skip it.

Flexibility over rigidity

Life doesn’t follow perfect categories. Your planner must bend, not break.

A good planner lets you:

- Add custom categories

- Adjust monthly budgets

- Track irregular expenses

- Change goals without guilt

Ever tried to “fit” your life into a planner that doesn’t fit you? Frustrating, right?

Room to reflect

The best simple budget planners include space to reflect. I love sections that ask questions like, “What worked this month?” or “What stressed you out?”

Reflection turns budgeting from punishment into growth. 🧠

Top types of simple budget planners that work

You don’t need one “perfect” planner. You need the right style for your brain. Here are the top options.

The classic paper budget planner

This is my personal favorite, no contest.

You write, you track, you adjust. It feels real.

Pros:

- Super simple

- No tech needed

- Builds strong habits

- Easy to customize

Cons:

- You must actually write daily

- No automatic calculations

I use mine every Sunday night for a monthly reset, and it keeps me grounded.

The basic spreadsheet planner 📊

If paper feels old-school, a Google Sheets budget can still stay simple.

Create just four columns:

- Date

- Description

- Category

- Amount

That’s it. No formulas needed unless you want them.

FYI, this works especially well for digital minimalists.

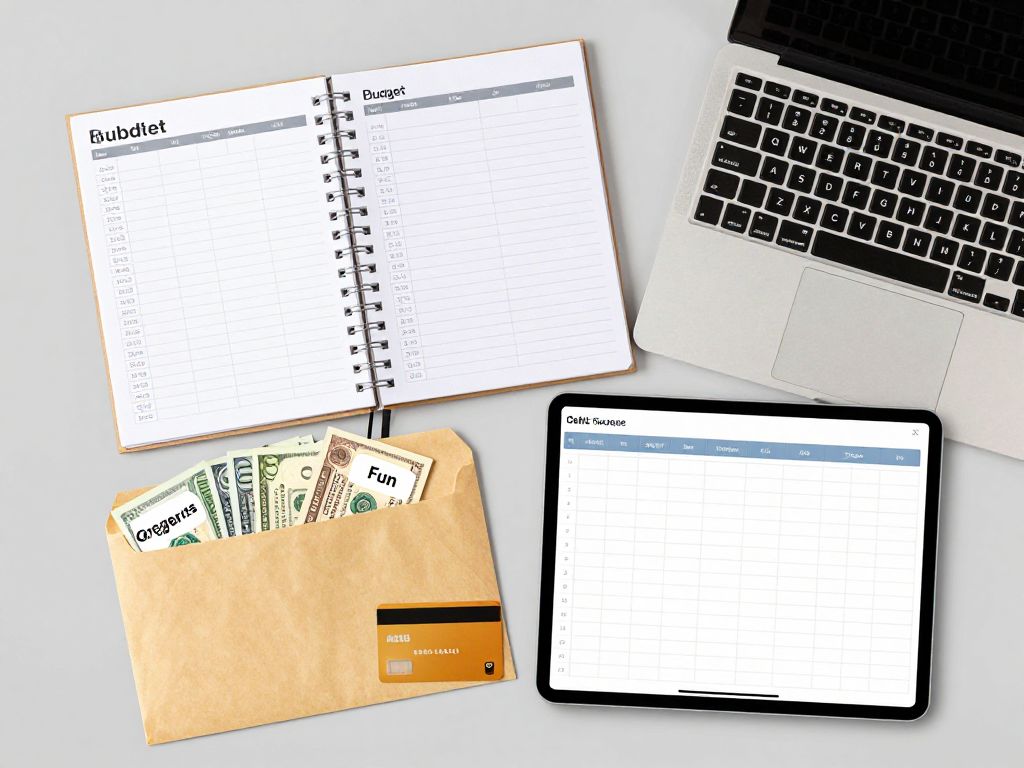

The envelope system planner 🧾

This is where budgeting gets tactile.

You label envelopes like:

- Groceries

- Fun

- Gas

- Eating out

Then you put cash inside. When the envelope empties, you stop spending. Simple, brutal, effective.

Ever watched your “fun money” disappear and thought twice about another $15 smoothie? Exactly.

The hybrid planner

This blends paper + digital.

You track daily spending in an app but plan monthly in a paper planner. Best of both worlds.

I use this when life feels busy but I still want structure.

How to pick your perfect simple budget planner

Don’t grab the prettiest one on Amazon just because it matches your water bottle.

Ask yourself three questions:

- Do I prefer writing or typing?

- Do I need structure or freedom?

- Do I want cash, cards, or both?

If you love writing, pick paper.

If you love tech, pick spreadsheet.

If you overspend, pick envelopes.

No drama, just honest answers.

How to actually use your planner step-by-step

Buying a planner means nothing if you don’t use it. Here’s my foolproof method.

Step 1 — Write your income first

List every dollar you expect to earn.

Include:

- Paychecks

- Side hustle money

- Bonuses

- Freelance payments

Be realistic, not optimistic.

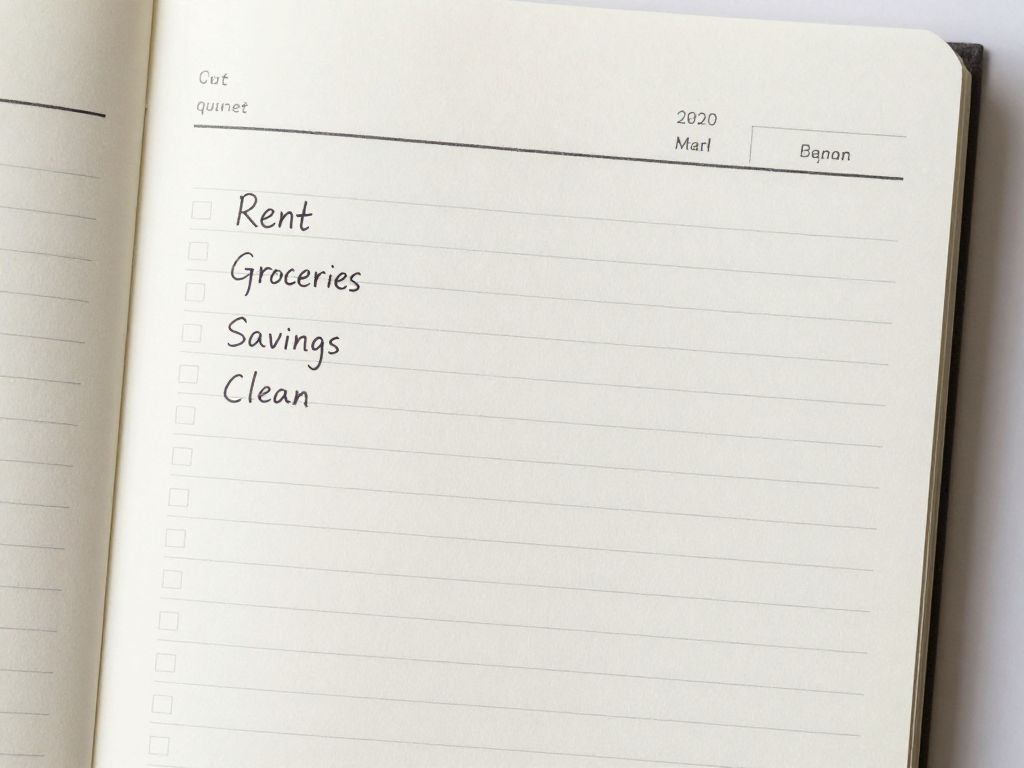

Step 2 — List fixed bills

Write every bill you must pay:

- Rent

- Utilities

- Phone

- Insurance

- Car payment

Circle these in bold because they come first. Bills before vibes.

Step 3 — Assign spending categories

Break your remaining money into categories like:

- Groceries

- Gas

- Fun

- Personal care

- Subscriptions

This is where simple budget planners shine.

Step 4 — Track daily spending

Every night, jot down what you spent. No excuses.

Bought coffee? Write it.

Ordered DoorDash? Write it.

Impulse shopped? Write it.

Painful? Maybe. Powerful? Absolutely.

Step 5 — Do a weekly check-in

Once a week, ask yourself:

- Am I on track?

- Did I overspend?

- Do I need to adjust?

Small tweaks beat big failures.

Common budgeting mistakes (and how to avoid them)

I’ve made all of these, so you don’t have to.

Mistake 1 — Being too strict

Budgets fail when they feel like jail. You need fun money, period.

Give yourself at least $50–$150 for guilt-free spending.

Mistake 2 — Forgetting irregular expenses

Birthdays, car repairs, and vacations will happen whether you plan for them or not.

Add a category called “sinking funds.” 🎯

Examples:

- Car maintenance

- Gifts

- Travel

- Medical

Mistake 3 — Not tracking small purchases

Those $5 coffees add up fast. I once spent $180 in a month on drinks without noticing. Yikes.

Track everything.

Mistake 4 — Giving up after one bad week

One messy week doesn’t mean failure. It means you’re human.

Adjust and keep going.

My favorite simple setup (real talk)

Here’s exactly what I use.

- Paper monthly planner

- Weekly spending log

- Envelope system for “fun money”

- Google Sheet for savings goals

Every Sunday, I sit with tea, my planner, and my bank app. I review, adjust, and reset. It feels calm, not stressful.

Ever tried turning budgeting into a cozy ritual instead of a chore? Highly recommend. ☕️

How to pair your planner with smart tools

Simple doesn’t mean alone. These add power without complexity.

Tool 1 — Automatic savings

Set up auto-transfer to savings on payday.

Even $50 per check builds momentum.

Tool 2 — Bill calendar

Mark bill due dates in your planner. No surprises, no late fees.

Tool 3 — Spending alerts

Turn on notifications for big purchases over $100.

You’ll stay aware without obsessing.

How to make budgeting stick long-term

Consistency beats perfection every time.

Habit tip 1 — Same time, same place

Pick one budgeting day per week. I pick Sunday night.

Habit tip 2 — Keep it simple

Don’t overcomplicate categories. 8–10 max.

Habit tip 3 — Celebrate wins

Hit a savings goal? Treat yourself within budget. 🎉

Habit tip 4 — Review monthly

At month’s end, ask:

- What went well?

- What felt hard?

- What will I change next month?

Growth > guilt.

Best simple budget planners you can try

Here are planner styles that consistently work for real people.

Option A — Minimal monthly planner

Best for beginners who hate clutter.

Features:

- One page income

- One page expenses

- Simple savings tracker

Perfect if you feel overwhelmed easily.

Option B — Detailed financial planner

Best if you love structure.

Includes:

- Debt tracker

- Sinking funds

- Net worth page

- Monthly goals

Great for serious money glow-ups.

Option C — Printable planner

Cheap, customizable, and flexible.

You print what you need and skip what you don’t. Smart and budget-friendly.

Why simple planners outperform apps

Apps can crash, update, or get deleted. Your planner won’t.

Writing creates accountability. You see your patterns. You own your choices.

And honestly, flipping pages feels way more satisfying than scrolling.

Ever felt proud crossing off a bill paid? That dopamine hit is real. ✨

Turning your planner into a money roadmap

Think of your planner as a GPS, not a rulebook.

It shows where you’ve been and where you want to go.

Your goals might include:

- $1,000 emergency fund

- Debt payoff

- Vacation savings

- New laptop

Write them big. Make them visible.

The mindset shift that makes budgeting easier

Stop thinking of budgeting as restriction. Start seeing it as freedom.

When you plan your money, you choose your life instead of reacting to bills.

That’s power, not punishment.

Conclusion: Your money, your rules

Simple budget planners don’t promise magic, but they deliver results. They help you track, adjust, and grow without overwhelm.

You don’t need perfection. You need consistency.

You don’t need fancy tech. You need clarity.

You don’t need shame. You need structure.

If you start this week, by next month you’ll feel calmer, clearer, and more confident with your dollars.

So grab a planner, pick a system, and take control. Your future self will thank you. 💖