How to Pay Off Debt When Living Paycheck to Paycheck

Let’s be real for a second. Living paycheck to paycheck while trying to pay off debt feels like running on a treadmill that never turns off. You run, you sweat, you try harder… and somehow you’re still in the same place. Sound familiar? Yeah, I’ve been there too, staring at my bank balance like it personally betrayed me.

The good news? You can pay off debt even when money feels painfully tight. No lottery wins required. No “just stop buying coffee” nonsense. Just real, doable steps that work in real life.

So grab a cup of chai or coffee ☕, and let’s talk this through—friend to friend.

Why Paying Off Debt Paycheck to Paycheck Feels Impossible (But Isn’t)

Living paycheck to paycheck messes with your head. Every dollar already has a job before it even lands in your account. Rent. Groceries. EMIs. Bills. And then debt sits there like an uninvited guest.

Ever wondered why advice online feels so useless sometimes? Because most tips assume you have “extra” money lying around. IMO, that advice lives in a fantasy world.

Here’s what actually makes it hard:

- No breathing room between paychecks

- One surprise expense = total chaos

- Debt payments feel like punishment instead of progress

But here’s the twist. Paying off debt paycheck to paycheck isn’t about having more money. It’s about using what you already have differently. That shift changes everything.

Step 1: Get Brutally Honest About Your Numbers

I know, I know. Numbers feel scary. But avoiding them doesn’t help—trust me, I tried 🙃.

List All Your Debts (Yes, All of Them)

Write everything down. No skipping.

- Credit cards

- Personal loans

- Buy-now-pay-later stuff

- Friend or family loans (awkward, but real)

Next to each debt, note:

- Total balance

- Interest rate

- Minimum payment

- Due date

This list feels uncomfortable at first. Then it feels powerful. Clarity beats anxiety every single time.

Step 2: Stop Aiming for “Debt Freedom” (Aim Smaller)

Here’s a hot take: Thinking about becoming debt-free can actually slow you down.

Why? Because it feels massive and exhausting.

Instead, focus on:

- Paying off one small balance

- Beating one due date

- Making one extra payment

Ever noticed how checking off a small win feels addictive? That’s momentum doing its thing.

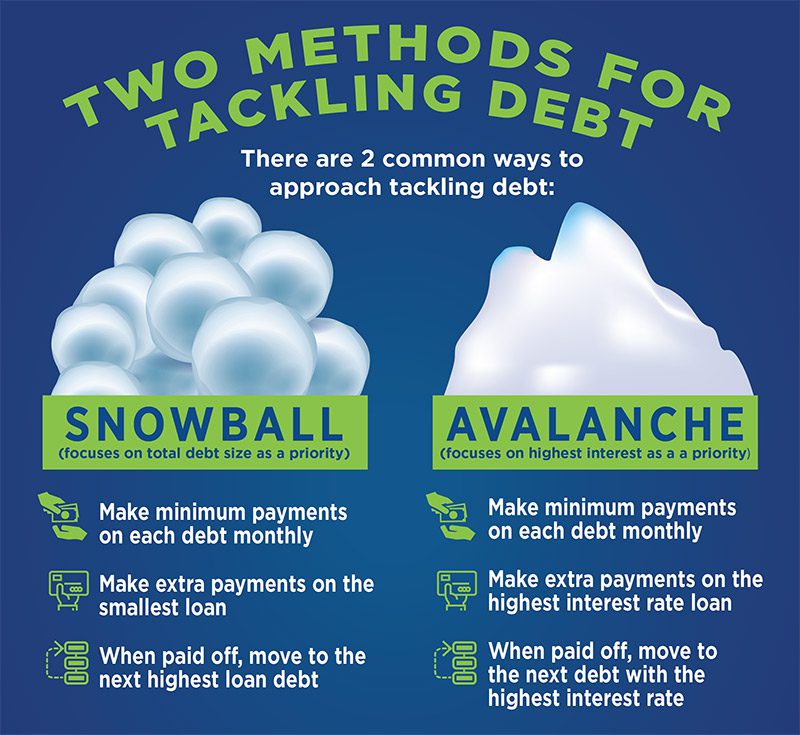

Step 3: Choose the Right Debt Strategy for Tight Budgets

You’ve probably heard of debt snowball and debt avalanche. Let’s talk real-life application.

Debt Snowball (My Go-To When Money Is Tight)

You pay off the smallest balance first, then roll that payment into the next debt.

Why it works paycheck to paycheck:

- You see progress fast

- Motivation stays high

- Less chance of quitting

Debt Avalanche (Mathematically Smarter, Emotionally Harder)

You attack the highest interest rate first.

Why it feels harder:

- Progress looks slow

- Motivation dips early

If motivation keeps you consistent, snowball wins. If discipline drives you, avalanche works. Pick the one you’ll actually stick with.

Step 4: Find “Hidden Money” Without Feeling Deprived

No, I’m not about to tell you to stop living your life. But most of us leak money without noticing.

Quick Wins That Don’t Hurt

Try these first:

- Cancel subscriptions you forgot about (they’re sneaky)

- Downgrade plans you barely use

- Switch to cheaper brands for basics

- Delay upgrades you don’t truly need

Even ₹1,000–₹2,000 extra per month can snowball into serious debt progress. Small money still counts—FYI.

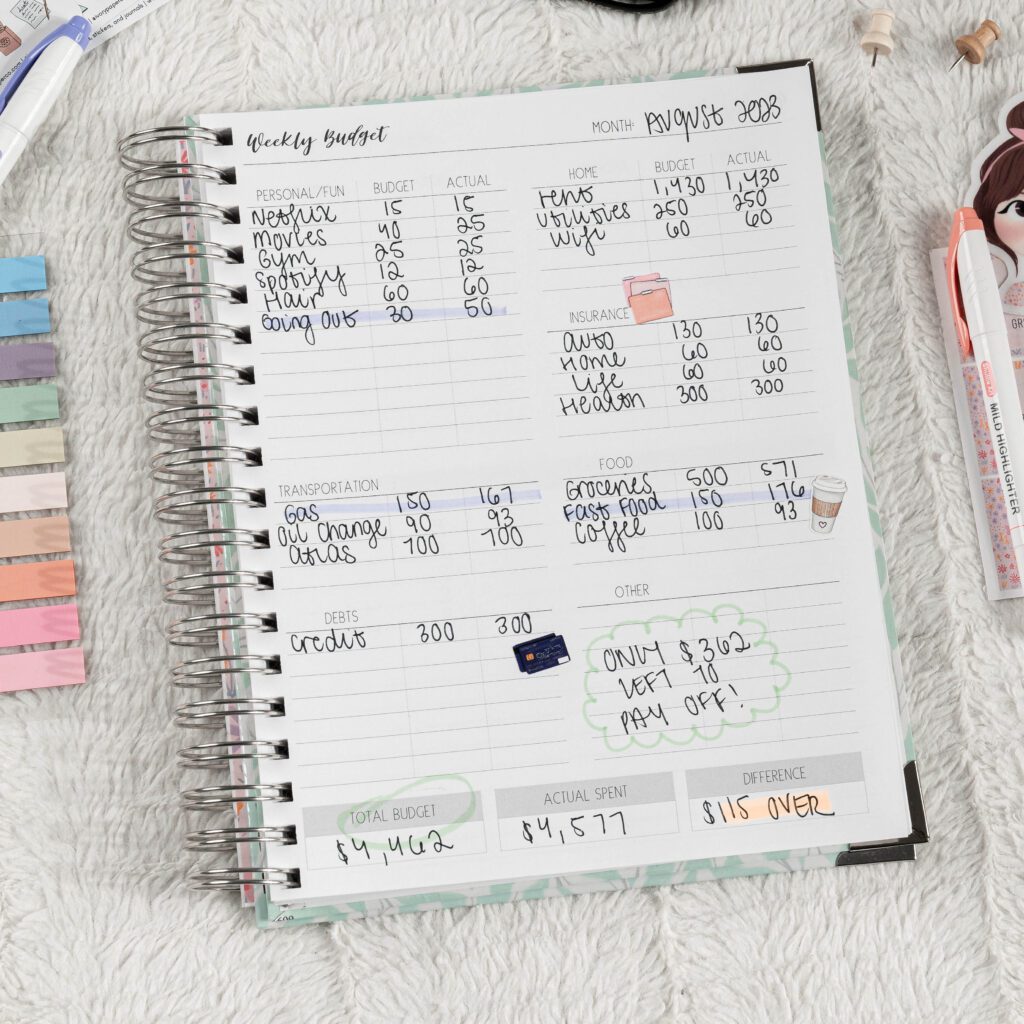

Step 5: Give Every Dollar a Job (Before It Disappears)

When you live paycheck to paycheck, unplanned money always vanishes. Always.

Try a Bare-Bones Budget (Just for Now)

This isn’t forever. This is survival mode.

Your budget covers:

- Essentials (rent, food, utilities)

- Minimum debt payments

- One small “life” category so you don’t snap

Then you assign:

- Any leftover money straight to debt

Think of it like this: If money doesn’t have a job, it quits on you.

Step 6: Build a Tiny Emergency Buffer (Yes, Even Now)

I used to think emergency funds were for rich people. Turns out, they’re for stressed people.

You don’t need thousands. Start with:

- ₹2,000

- ₹5,000

- One week of expenses

Why this matters:

- Emergencies stop creating new debt

- You stop relying on credit cards

- Progress stops resetting to zero

This step feels boring. It also saves your sanity.

Step 7: Lower Your Minimum Payments (Legally)

This part feels sneaky, but it’s smart.

Call Your Lenders

Ask about:

- Lower interest rates

- Temporary hardship programs

- EMI restructuring

- Fee waivers

Worst case? They say no. Best case? You free up cash for faster payoff.

I once shaved a few thousand off my monthly payments with one phone call. Best 15 minutes I ever spent.

Step 8: Increase Income (Without Burning Out)

I won’t say “just get a second job.” That advice ignores reality.

Instead, think small and flexible.

Low-Stress Ways to Boost Cash

- Freelance skills you already have

- Weekend or short-term gigs

- Selling unused items at home

- Cashback and rewards optimization

Even temporary extra income aimed only at debt can shorten your payoff timeline massively.

Step 9: Automate What You Can (Protect Your Willpower)

Willpower runs out. Automation doesn’t.

Set up:

- Automatic minimum payments

- Automatic extra payments right after payday

Why after payday? Because you can’t spend what you never see. Sneaky? Maybe. Effective? Absolutely 🙂

Step 10: Prepare for Bad Months (Because They Will Happen)

Some months will suck. Bills pile up. Motivation disappears. Life happens.

When that happens:

- Don’t quit

- Don’t spiral

- Don’t add new guilt

Instead:

- Pay minimums

- Pause extra payments

- Resume when things stabilize

Consistency beats perfection. Every time.

Step 11: Stop Comparing Your Journey to Others

Social media makes debt payoff look glamorous. It isn’t.

Some people:

- Earn more

- Have family support

- Started earlier

You focus on:

- Your progress

- Your pace

- Your reality

Comparison drains energy you need to win this.

Step 12: Track Progress Like a Game

Progress feels invisible unless you track it.

Try:

- Coloring charts

- Apps

- Simple notes in your phone

Seeing balances drop—even slowly—keeps you going when motivation fades.

The Truth About Paying Off Debt Paycheck to Paycheck

Here’s the honest truth nobody says out loud:

Paying off debt paycheck to paycheck feels unfair, slow, and exhausting.

And yet, it works if you stick with it.

You don’t need perfection.

You don’t need huge income jumps.

You need patience, consistency, and a plan that respects your reality.

Final Thoughts: You’re Not Bad With Money—You’re Just Human

If you remember one thing, remember this: Living paycheck to paycheck doesn’t mean you failed. It means you’re trying in a tough system.

You can pay off debt paycheck to paycheck.

You can rebuild control.

You can breathe again.

Start small. Stay consistent. Laugh at the chaos when you can. And keep going—even on messy months.

Because one day, you’ll look back and think, “Wow… I actually did it.” And that moment? Totally worth it 💪