How to Pay Off Debt Fast on a Low Income

Ever stared at your bank balance and your debt total at the same time and thought, “Wow… rude”? Yeah, same. Paying off debt feels hard enough, but trying to pay off debt fast on a low income can feel like running a marathon in flip-flops. Still, I promise you this: it is possible, and you don’t need a six-figure salary or monk-level discipline to make it happen 😊

I’ve been in that place where every rupee (or dollar) already had an assignment, and debt still demanded more. This guide comes from that reality—not from some fantasy land where “just earn more” magically solves everything. Let’s talk real strategies that actually work when money feels tight.

Why Paying Off Debt on a Low Income Feels So Brutal

Let’s be honest for a second. Low income doesn’t mean low effort. It usually means you already squeeze every bit of value out of your money.

You face problems like:

- No extra cash at the end of the month

- Unexpected expenses that wreck your plans

- Debt payments that eat your peace of mind

Sound familiar? Ever wonder why debt feels heavier when income stays low? Because margin matters, and you don’t have much of it. The goal here focuses on creating margin—even small ones—so you can attack your debt faster.

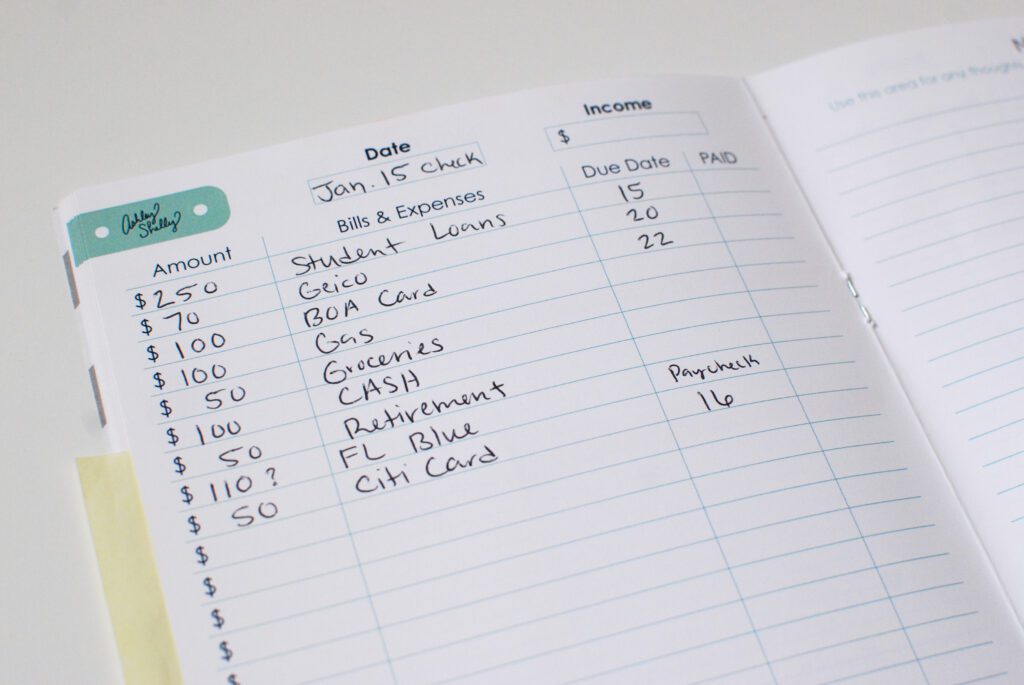

Get Crystal Clear on Your Debt (No Hiding Allowed)

I know, I know. Looking at all your debts at once feels like staring into the sun. Still, clarity beats anxiety every time.

List Everything You Owe

Grab a notebook or open a notes app and write down:

- Creditor name

- Total balance

- Interest rate

- Minimum payment

Yes, write it all down. This step gives you control back. IMO, avoiding numbers only gives debt more power.

Pick a Debt Payoff Method That Fits Your Brain

You’ve got two popular options:

- Debt Snowball: Pay off the smallest balance first for quick wins.

- Debt Avalanche: Pay off the highest interest first to save more money long term.

I prefer the snowball method on a low income. Those early wins feel motivating, and motivation keeps you consistent. Ever notice how momentum changes everything?

Build a Bare-Bones Budget That Actually Works

Forget fancy spreadsheets. You need something simple enough to stick with when life gets messy.

Focus on the “Survival First” Budget

Start with just three categories:

- Essentials: Rent, food, utilities, transport

- Minimum debt payments

- Everything else

That’s it. Keep it boring. Fancy budgets fail when income stays tight.

Track Spending Like a Hawk (But Don’t Obsess)

For one month, track every expense. Every chai, snack, and impulse buy counts.

This step shows you:

- Where money leaks happen

- Which expenses don’t add much value

FYI, awareness alone often frees up cash without cutting joy :/

Cut Expenses Without Making Life Miserable

I hate advice that says, “Cut everything fun.” That strategy burns out fast.

Target the Big Wins First

Focus on expenses that actually move the needle:

- Housing: Roommates, renegotiating rent, downsizing

- Transport: Public transport, carpooling, selling a second vehicle

- Subscriptions: Cancel anything you forgot you even had

Saving ₹2,000 on rent beats skipping coffee for six months. Ever tried canceling subscriptions and felt instant relief?

Use the “Value Test” on Small Expenses

Ask yourself one question before spending:

“Does this genuinely make my life better?”

If the answer feels like “meh,” skip it and redirect that money toward debt.

Increase Your Income (Without Burning Out)

Cutting expenses has limits. Income, however, has upside.

Start with Low-Energy Side Hustles

You don’t need a second full-time job. Look for things that fit your schedule:

- Freelance writing or design

- Online tutoring

- Selling unused items

- Microtasks or weekend gigs

I once sold random stuff lying around and knocked out a small debt in weeks. Was it glamorous? Nope. Did it work? Absolutely.

Send Extra Income Straight to Debt

Here’s the rule: no lifestyle upgrades until debt disappears.

Every bonus, side hustle rupee, or cash gift should go directly to your current target debt. Why delay freedom?

Use Smart Debt Hacks to Speed Things Up

When income stays low, strategy matters even more.

Call Your Creditors (Yes, Seriously)

Pick up the phone and ask for:

- Lower interest rates

- Fee waivers

- Temporary hardship programs

Worst case, they say no. Best case, you save thousands. Why not ask?

Consider Balance Transfers or Consolidation

If you qualify, these options can:

- Lower interest

- Simplify payments

- Speed up payoff timelines

Just promise yourself one thing: don’t add new debt while using them. That defeats the whole point.

Build a Tiny Emergency Fund (Even While in Debt)

I know this sounds counterintuitive, but hear me out.

Without a buffer, every emergency sends you back into debt. That cycle keeps people stuck forever.

Aim for a Starter Fund First

Save ₹5,000–₹10,000 (or one month of essentials). Keep it separate.

This fund:

- Stops panic borrowing

- Protects your progress

- Gives mental peace

Ever felt calmer just knowing you had backup money? That feeling matters.

Stay Motivated When Progress Feels Slow

Debt payoff on a low income isn’t fast every week. Some months crawl.

Track Progress Visually

Use:

- Debt payoff charts

- Thermometers

- Apps or spreadsheets

Watching balances drop—even slowly—keeps you going.

Celebrate Small Wins (Without Spending)

Paid off a debt? Celebrate with:

- A movie night at home

- A long walk with music

- A guilt-free nap

Reward progress without undoing it. Smart, right?

Avoid Common Mistakes That Keep You Stuck

Let’s save you some frustration.

Don’t Wait for “More Money”

People say, “I’ll start when I earn more.” That day rarely arrives.

Start with what you have. Momentum beats perfection every time.

Don’t Compare Your Journey

Someone online will always pay off debt faster. Ignore them.

Different income, different life, different responsibilities. Focus on your lane.

How Long Does It Really Take?

This depends on:

- Total debt

- Interest rates

- Extra payments

Still, consistent effort almost always beats aggressive plans that collapse. Even small extra payments compound over time.

Ever notice how progress sneaks up on you? One day, you suddenly owe less than you imagined.

Sample Simple Plan to Pay Off Debt Fast on a Low Income

Here’s a realistic roadmap:

- List all debts clearly

- Build a survival budget

- Save a tiny emergency fund

- Pick snowball or avalanche

- Cut high-impact expenses

- Add small income streams

- Throw every extra rupee at debt

- Repeat monthly

Simple doesn’t mean easy, but simple works.

Final Thoughts: You’re Not Broken, the System Is

Debt on a low income doesn’t mean you failed. It means you’re navigating a tough system with limited resources.

If you stay consistent, stay honest, and stay patient, you will see results. I’ve watched it happen for myself and for others who refused to quit.

So, what’s your next move—listing your debts or canceling that forgotten subscription? Start small tonight. Future you will seriously thank you 💪