Money Habits That Keep You Living Paycheck to Paycheck

You’re not bad with money. You’re just juggling rent, groceries, and that one bill that always shows up early like an overachiever. Living paycheck to paycheck feels like running on a treadmill that randomly speeds up. You don’t need a lecture. You need habits that work when your budget has zero chill. Let’s talk practical moves you can actually do this week.

Know Your Real Number (Not the Fantasy One)

Budgets fall apart because they start with lies. Not big ones—just “I’ll only spend $40 on food this week” lies. Stop. Track what you actually spend for two weeks. Then average it.

Build your baseline:

- List your fixed bills: rent, utilities, phone, transportation, minimum debt payments.

- Add your “life” costs: groceries, gas, pet stuff, toiletries.

- Include the sneaky ones: subscriptions, gifts, haircuts, school fees, seasonal expenses.

Now you’ve got your survival number: the amount you must cover every month. That’s the number you protect first. Everything else negotiates for space in your budget like a reality TV audition.

Use a paycheck-based plan

Align bills with your paychecks:

- Split monthly bills in half and assign to each paycheck.

- Set bill due dates to match your pay schedule (most companies will change them if you ask).

- Automate the non-negotiables the day after you get paid to remove temptation.

Simple? Yes. Boring? Also yes. Effective? Absolutely.

Prioritize Like a CFO (Who Drinks Store-Brand Coffee)

When money’s tight, every dollar needs a job. The order matters. Think survival first, future second, nice-to-haves last.

Pay in this order:

- Housing and utilities

- Transportation to work (or essential errands)

- Groceries and basic needs

- Minimum debt payments

- Everything else

Missed a minimum payment before? It hurts your credit and can trigger fees. IMO, preserve your credit score while you build stability. It makes everything cheaper later.

The “bare-bones” week

When you’re in a tight stretch, run a 7-day bare-bones challenge:

- No delivery. No takeout. Leftovers become a personality trait.

- Use what’s already in your pantry and freezer.

- Pause streaming (most services let you pause instead of cancel).

One week won’t fix everything—but it buys you breathing room.

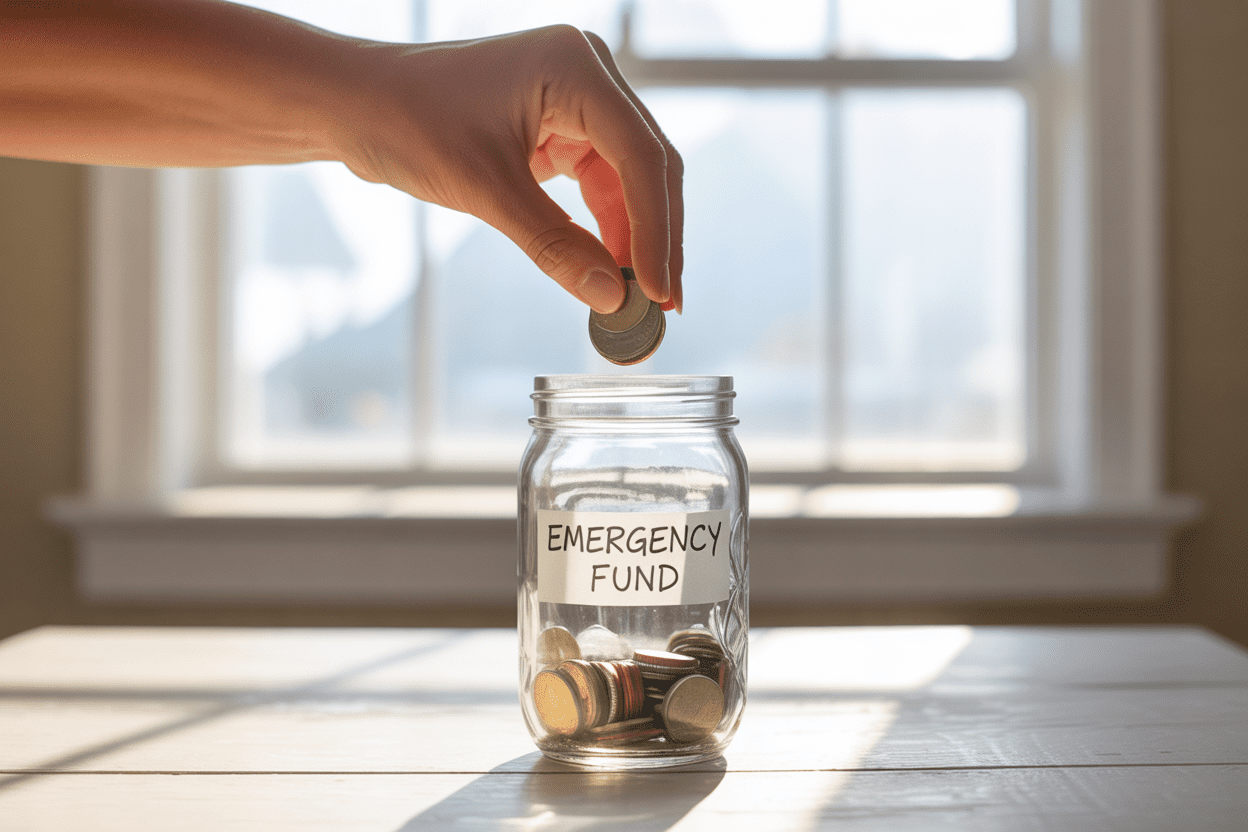

Build a Micro-Buffer (Your Tiny Financial Force Field)

You don’t need a 3-month emergency fund right now. You need $150–$500 in a checking buffer. It stops overdraft fees and “oops” moments.

How to build it without hating life:

- Skim $10–$25 from each paycheck. Automate it to a separate “Buffer” sub-account.

- Siphon refunds, cash-back, and unexpected $20s into it.

- Sell one clutter item weekly: old tech, shoes, hobby gear.

When an expense hits early or a bill surprises you, your buffer catches it. FYI, buffers reduce stress more than any budgeting app on earth.

Then move to a $500-$1,000 emergency stash

Keep this in a high-yield savings account (separate from checking). Name it something dramatic like “Do Not Touch, Future Me” because, let’s be honest, that helps.

Make the Big 3 Cheaper (Without Going Full Hermit)

You don’t need to quit joy. You need to negotiate the boring bills and streamline the costly habits.

Focus here first:

- Food: Plan three go-to meals. Shop from a list. Buy store brands. Batch-cook cheap proteins (chicken thighs, beans, eggs). Keep “emergency” convenience food on hand so you don’t order DoorDash at 10 p.m.

- Phone/Internet: Ask for a loyalty discount, switch to a cheaper plan, or qualify for low-income programs. It’s one call. It can save $20–$60/month.

- Transportation: Combine errands, carpool once a week, or use transit for short trips. If your car insurance hasn’t been shopped in 12 months, do it—multi-quote sites exist for a reason.

Trim the subscriptions quietly draining you

Do a 30-minute audit:

- List every subscription (app store + bank statement).

- Cancel anything you haven’t used in 30 days. Pause the “maybes.”

- Rotate entertainment: one service per month instead of five simultaneously.

Boom. Found money.

Debt: Keep It Simple, Keep It Moving

Debt can feel like quicksand, but you don’t need a spreadsheet worthy of NASA. Make steady, confident moves.

Pick one method and commit:

- Snowball: Pay off the smallest balance first for a fast win. Great for motivation.

- Avalanche: Pay the highest interest first to save money. Great for math nerds.

Either way, pay minimums on everything else, then throw extra at your chosen target. When you finish one, roll that payment into the next. Momentum becomes your friend.

Negotiate and consolidate (strategically)

- Call and ask for a lower APR. You’d be surprised how often it works.

- Transfer to a 0% intro APR card if you can commit to paying it down before the promo ends.

- If payments feel impossible, talk to a nonprofit credit counseling agency. They can reduce interest and set up a plan without trashing your credit.

Give Your Dollars a Job Before They Even Arrive

Waiting until payday to decide where money goes is like grocery shopping hungry. You know how that ends.

Use a paycheck plan:

- Pre-assign money to bills, food, gas, debt, and a tiny fun amount.

- Set up automatic transfers for bills and savings. You can always adjust manually if needed.

- Use “envelopes” (digital or literal) for categories that get slippery—food, gas, spending.

Not a fan of apps? Use the “two-checking account” trick:

- Account A: Bills only. Direct deposit a set amount here.

- Account B: Variable spending. This is your daily card.

When Account B runs low, you stop spending. Training wheels for adults, and honestly, it works.

Make More Money (Yes, Even a Little Helps)

Cutting expenses hits a wall. Income doesn’t. Even $100–$300 extra per month changes everything.

Small, realistic boosts:

- Overtime or an extra shift twice a month

- Seasonal work for a few weeks (holidays = money)

- Freelance your skills: babysitting, tutoring, pet-sitting, delivery apps, basic design, translation

- Sell clutter on local marketplaces—set a weekly “sell one thing” reminder

Use extra money with intention:

- 50% to buffer/emergency fund

- 30% to debt

- 20% to joy or needs you postponed

Reward yourself a little so you stick with it. We’re building habits, not punishment.

Ask for the raise

You don’t need to deliver a TED Talk. Try: “Based on my contributions (insert specific wins), I’d like to discuss aligning my compensation with my responsibilities.” Practice once. Send the email. Worst case, you get feedback and a timeline.

Prevent Money Emergencies with Boring Systems

You don’t need heroic discipline when you have guardrails.

Set up simple defaults:

- Auto-pay minimums on all debts to avoid fees. You can make extra payments manually.

- Calendar reminders for bill due dates and renewal periods.

- Sinking funds for irregular expenses: car maintenance, vet visits, annual fees, gift season. Toss in $10–$30 per paycheck.

And please, for the love of your sanity, put a sticky note on your debit card: “Check balance first.” Two seconds that can save you $35.

Mindset: Progress, Not Perfection

Perfection kills more budgets than Starbucks ever will. You will mess up sometimes. That’s normal. The goal is fewer mess-ups and faster recoveries.

Try these mental shifts:

- Think in weeks, not months. Shorter timelines feel doable.

- Celebrate small wins: “Paid every bill on time.” “Cooked four nights.”

- Use a tiny “fun money” line—$10–$25. Deprivation backfires.

If you slip? Reset with the next paycheck. No shame spiral needed. IMO, shame is the most expensive emotion in personal finance.

FAQ

Should I save or pay off debt first?

Build a tiny buffer ($150–$500) first so you stop bleeding fees and overdrafts. Then pay minimums plus extra on your chosen debt target while slowly growing savings. When you hit $500–$1,000 in savings, you can focus harder on debt.

How do I budget when my income varies?

Base your plan on your lowest predictable income. Cover essentials with that, and treat extra income as “bonus” to fund savings, debt, and irregular expenses. Keep one month of bare-bones expenses in your checking buffer as your goal—it smooths the bumps.

What if I can’t afford all my bills this month?

Prioritize housing, utilities, food, and transportation. Then call lenders and service providers to ask for hardship plans, payment extensions, or due date changes. Document every call. Pay something, even small amounts—it keeps accounts in better standing while you stabilize.

Do budgeting apps actually help?

Apps help if you use them daily for 60 seconds. The tool matters less than the habit. If you hate apps, use two accounts and a notes app. If you love apps, try one with envelope-style categories and paycheck scheduling. Pick the simplest system you’ll stick to.

How can I stop impulse spending?

Use a 24-hour rule for non-essential purchases. Keep “wishlist” items in your cart for a week. Unsubscribe from promo emails. Leave your card at home when possible and take cash for discretionary spending. And eat before you shop—hunger is a menace.

Is credit card rewards worth it while living paycheck to paycheck?

Only if you pay in full every month. If you carry a balance, interest eats any rewards and then some. Focus on stability first. Rewards can wait.

Conclusion

You don’t need perfect discipline or a six-figure income. You need a few smart systems, a small buffer, and the stubborn belief that you can make progress even when it’s slow. Give your dollars jobs, protect the essentials, and make tiny upgrades every paycheck. Consistency beats intensity. You’ve got this—one boring, powerful habit at a time.