How to Plan Money Goals Without Overwhelm: Simple Steps to Start Now

I get it. Money goals can feel like dieting for your wallet: everyone pretends it’s easy, but you end up craving ice cream and wondering where your budget went. Let’s cut the fluff and map out goals that actually stick. Quick truth: you don’t have to overhaul your life to make real progress. You just need a plan that fits your reality and a little momentum.

Know what you’re aiming for without turning it into a stress test

When you say “money goals,” what you’re really saying is “I want more control, less drama, and maybe a little freedom.” Start with clarity, not guilt. Ask yourself: what would I do differently if money were not a constant source of anxiety? Maybe it’s a safety net, maybe it’s a trip, or maybe it’s finally paying off that thumb-tudor debt you’ve been eye-rolling about.

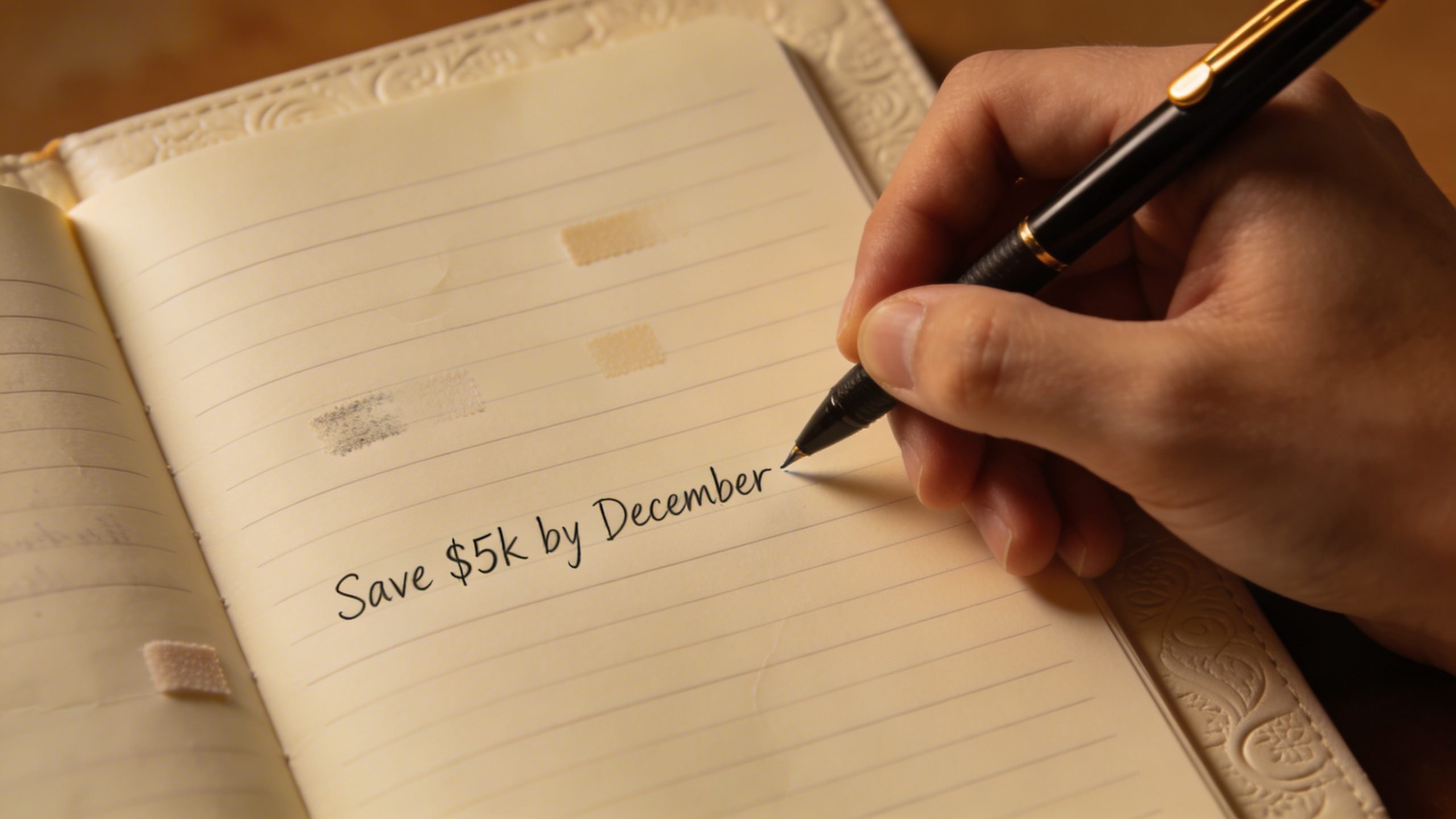

– List your top three goals. Be specific: “Save $5k for emergency fund by December” beats “save more money.”

– Attach a rough timeline. A deadline turns wishes into action.

– Name the metric you’ll track. Months of no-spend? Percentage of income saved? Pick something concrete.

FAQ:

Why keep goals small at first?

Small goals build confidence and momentum. Tiny wins stop money anxiety from spiraling into paralysis. Think micro-goals that are easy to hit, then stack up.

What if my life is chaotic right now?

Start with adjustments you can live with. You’ll thank yourself later when a bump in income or an expense cut doesn’t derail everything.

Is it okay to redo goals?

Absolutely. Goals aren’t rules carved in stone. If life shifts, tweak the numbers and keep going. IMO adaptability beats rigidity any day.

Break the plan into bite-sized steps

Big plans fail when they feel like quests to Mordor. Break them into tiny, doable steps you can actually complete without losing your mind.

– Step 1: Block 15 minutes a week to review money. That’s it. No marathon sessions required.

– Step 2: Identify one (yes, one) expense to cut or reduce. The socks-off factor happens when you prove you can do this repeatedly.

– Step 3: Automate where possible. Set up automatic transfers to savings or debt payments so you don’t have to rely on willpower alone.

– Step 4: Create a simple tracking sheet. A glance should tell you if you’re on track or not.

Subsection:

Automation as your best friend

Automations aren’t cheating; they’re nudges that honor your goals without guilt trips. Make a small monthly transfer the moment you’re paid. You’ll stop the “where did all my money go?” mystery every time.

Align goals with real-life constraints (and a little humor)

Money goals work best when they fit your actual life—not some Pinterest-perfect version of it. Be honest about expenses, stress points, and your appetite for sacrifice.

– Honor fixed costs first: rent, utilities, debt minimums. They aren’t optional.

– Build a buffer for the fun stuff: a tiny “fun fund” keeps you from rebelling with a weekend spree.

– Plan for irregular income if you’ve got it. A little cushion goes a long way when your paycheck plays hide-and-seek.

– FYI: avoid all-or-nothing thinking. You don’t need to strip your life to the bone to win.

Subsection:

How to handle big goals without freaking out

Break big goals into monthly targets. If you want to save $10k in a year, that’s roughly $833 a month. But you don’t have to hit the full number from day one. Start with $200, then go up as you adjust.

Turn your goals into a budget that feels good

A budget doesn’t have to feel like a cage. It’s a map to your priorities, and it should leave room for a little joy.

– Create three buckets: Essentials, Goals, Fun.

– Essentials cover rent, groceries, transport. No negotiation there.

– Goals include retirement, debt, and emergency fund.

– Fun is your ruler’s break: one treat per week keeps you sane.

– Use a 50/30/20-ish approach as a starting point, then tailor it. The most effective budget is the one you actually use.

Practical budgeting tips

– Automate savings and debt payments first, then budget the rest.

– Round up expenses where possible. If you pay $4.68 for a coffee, round to $5 and stash the extra 32 cents.

– Review every month, not once a year. Small adjustments beat big regrets.

Master the art of saying no (to yourself and others) gracefully

You’ll encounter invitations to spend: a sponsored trip, a flash sale, a last-minute upgrade. You don’t have to say yes to everything. You just have to be honest.

– Develop a default reaction: “I can’t commit to that right now.” Then offer a better-aligned alternative.

– Reframe “no” as a choice with better options. “I’ll save that $50 for my emergency fund instead.”

– Communicate your goals to your circle. Accountability helps—friends who respect your priorities will, too.

Subsection:

When social pressure hits

Plan ahead for common triggers. If you know a friend loves spontaneous dinners, suggest a cheaper meet-up or set a monthly budget for outings. FYI, you’ll still have fun without draining your wallet.

Track progress without turning it into a freaky numbers game

Tracking is useful, but it can become a fixation. Keep it light, consistent, and practical.

– Choose 2-3 metrics max. Do not chase every shiny number.

– Use a simple dashboard: auto transfers, balance changes, debt paid off.

– Reflect, don’t berate yourself. If you missed a month, ask what happened and adjust.

– A quick cadence helps: review on the 1st and 15th of each month.

Simple tracking tools that work

– A basic spreadsheet with sum totals.

– A budgeting app that auto-categorizes expenses.

– A handwritten notebook if you crave tactile feedback.

FAQ

How long should it take to see results?

Results vary, but you should notice less stress and clearer numbers within 4–8 weeks. Momentum compounds fast when you automate and adjust, not punish yourself.

What if I have debt I want to tackle?

Tackle it with a plan that fits your life. Minimums + a small extra toward the highest-interest debt often works. If you can, automate the extra payment. It’s the small wins that add up to big relief.

Is it okay to change goals mid-year?

Yes. Life happens. Reassess every few months and adjust. The point is progress, not perfection. IMO, flexibility beats stubbornness.

How do I stay motivated without burning out?

Keep goals meaningful and visible. Post a note on your fridge, celebrate tiny wins, and keep a “why” ledger. If you feel overwhelmed, scale back temporarily and build back up.

Conclusion

Money goals don’t have to feel like a chore list that haunts you on weekends. Start with clarity, slice the work into tiny steps, and align your plan with real life. Automate the boring stuff, say no with charm, and track only what actually moves the needle. Before you know it, you’ll look up and realize you’ve built something sustainable, sane, and surprisingly enjoyable. So, what’s the first tiny step you’re taking this week to move toward your money goals?