Financial Planning for Beginners Explained Simply

Let me guess—you’ve Googled financial planning for beginners because money feels confusing, a little intimidating, and mildly judgmental 😅. You earn, you spend, and somehow your bank balance still plays hide-and-seek. Been there. I’ve absolutely been there.

The good news? Financial planning doesn’t require a finance degree, a fancy spreadsheet addiction, or giving up coffee forever. You just need a simple system, a bit of patience, and the willingness to start—even if your first step feels tiny.

So grab a coffee (yes, you can keep it), and let’s talk money like normal humans.

What Financial Planning Really Means (No Jargon, I Promise)

Financial planning sounds serious, right? Like something people in suits whisper about. In reality, financial planning means deciding what you want your money to do before it disappears.

That’s it. No drama.

Think of It Like This

You already plan things every day. You plan meals, trips, and even weekend naps. Financial planning just asks you to do the same thing with dollars.

At its core, financial planning for beginners answers a few basic questions:

- Where does my money come from?

- Where does my money go?

- What do I want my money to do next?

Once you answer those, the fog starts to lift. Ever noticed how clarity alone reduces stress? Yeah, money works the same way.

Why Beginners Struggle With Financial Planning (And It’s Not Your Fault)

Most people don’t struggle because they’re bad with money. They struggle because nobody taught them. Schools taught algebra, not budgeting. Thanks… I guess?

Common Beginner Mistakes I’ve Made Too

- Ignoring bank statements because vibes felt better than numbers

- Thinking budgeting meant “no fun allowed”

- Believing I needed more income instead of better planning

Sound familiar? You’re not broken. You’re just early in the process.

FYI: Financial planning rewards consistency, not perfection. Messy progress still counts.

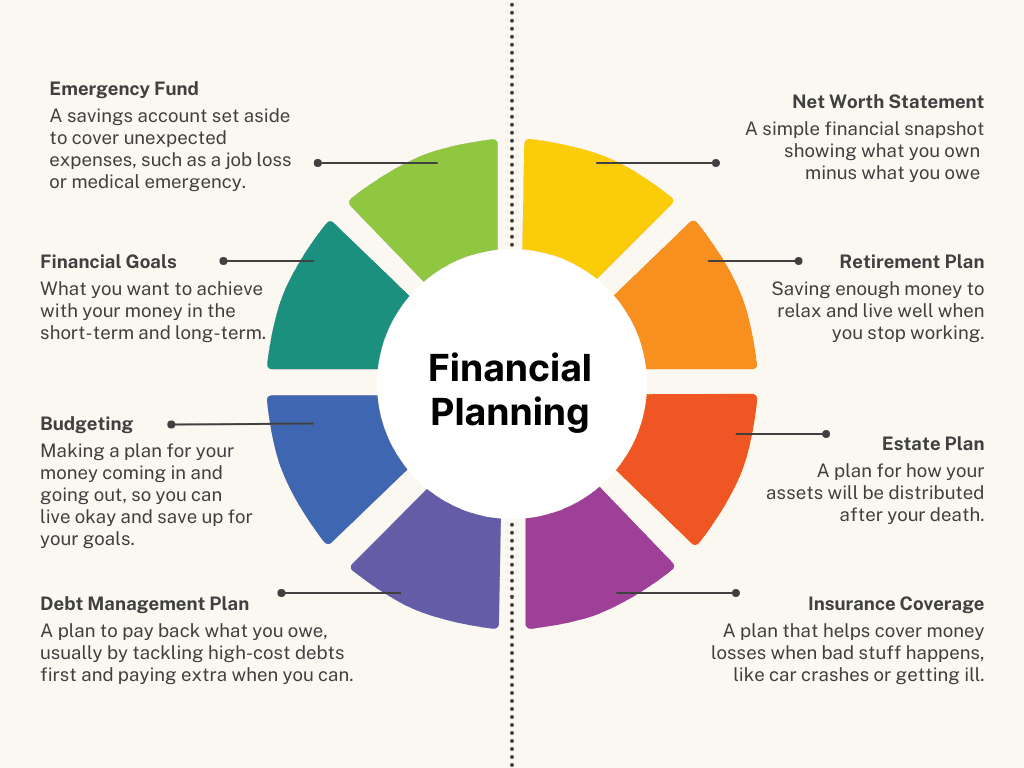

Step 1: Know Your Numbers (Yes, All of Them)

I won’t sugarcoat this. You must look at your numbers. Avoiding them doesn’t make them nicer.

Start With These Three Basics

- Monthly income: Salary, side hustle, freelance—everything

- Fixed expenses: Rent, utilities, insurance, subscriptions

- Variable spending: Food, gas, fun stuff, random Amazon regrets

Write them down. Use an app, a spreadsheet, or an old-school notebook. I started with a notes app and zero shame.

Once you see the full picture, things click fast. Ever wonder why money feels tight even with decent income? Numbers explain everything.

Step 2: Build a Beginner-Friendly Budget (Not a Prison Sentence)

Let’s kill a myth real quick. Budgets don’t restrict your life—they protect it.

I used to think budgets ruined fun. Turns out, not knowing my limits ruined fun way faster.

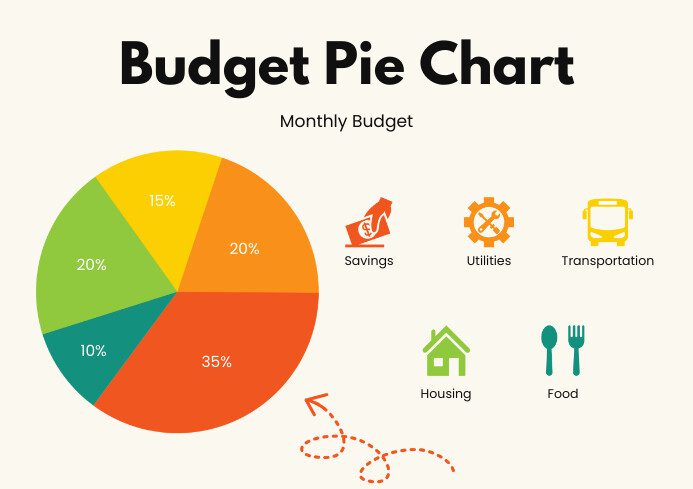

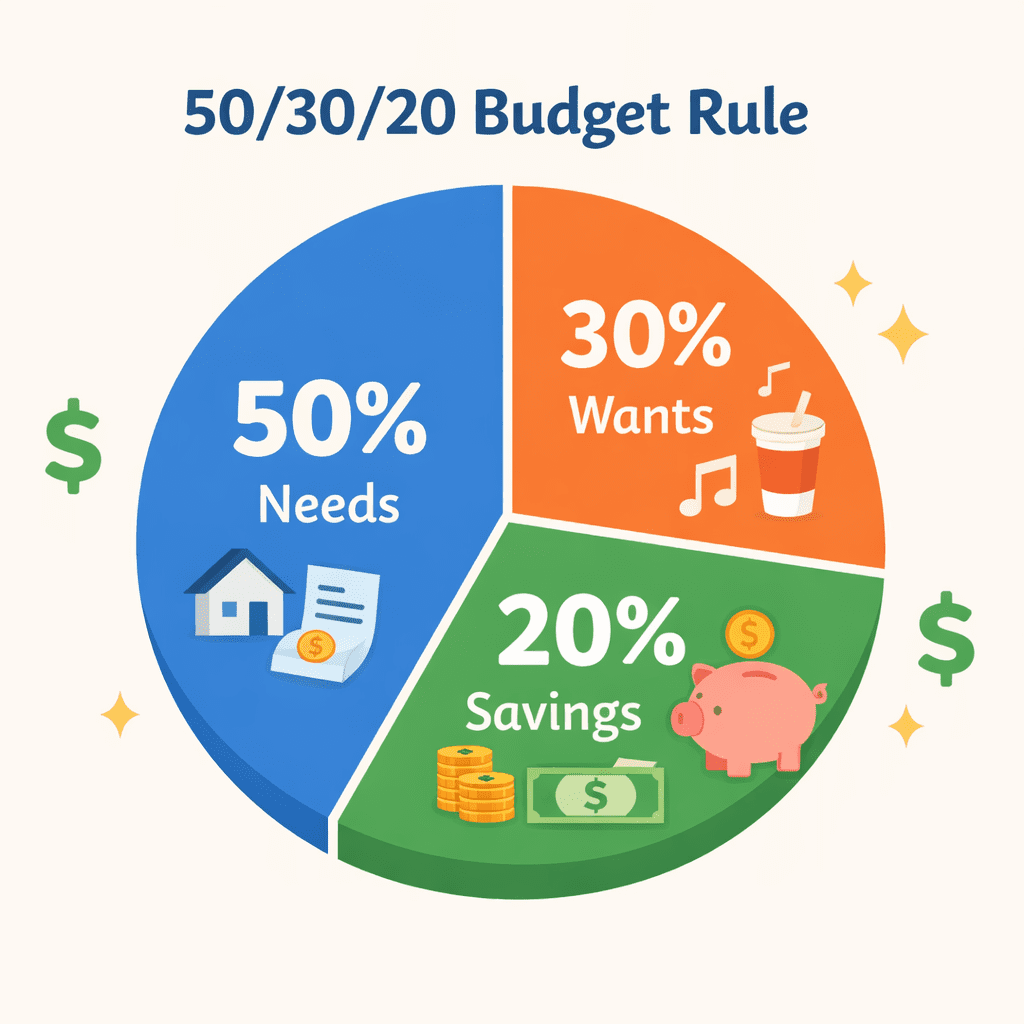

The Simple 50/30/20 Rule

This rule works beautifully for financial planning for beginners:

- 50% Needs: Rent, groceries, bills

- 30% Wants: Eating out, hobbies, entertainment

- 20% Savings: Emergency fund, investing, debt payoff

Adjust the percentages if needed. Real life isn’t a math problem. IMO, flexibility beats rigidity every time.

Why This Works

- You give every dollar a job

- You avoid overspending guilt

- You save without feeling deprived

Ever noticed how rules feel easier when they actually make sense?

Step 3: Emergency Funds—Your Financial Seatbelt

An emergency fund sounds boring until life throws a surprise bill at your face. Then it feels magical.

What an Emergency Fund Covers

- Car repairs

- Medical bills

- Job loss

- Life being… life

Aim for $1,000 first, then build toward 3–6 months of expenses. You don’t need to do this overnight.

I started with $25 a week. Slow? Yes. Effective? Absolutely.

Bold truth: Emergency funds turn panic into inconvenience. That alone makes them worth it.

Step 4: Tackle Debt Without Hating Your Life

Debt happens. Credit cards, student loans, personal loans—welcome to adulthood.

The goal isn’t shame. The goal is strategy.

Two Beginner-Friendly Debt Methods

- Snowball Method

- Pay smallest debt first

- Gain momentum fast

- Great for motivation

- Avalanche Method

- Pay highest interest first

- Save more money long-term

- Requires patience

I used the snowball method because early wins kept me sane :). Choose the method you’ll actually stick with.

Ever notice how emotional momentum matters more than math sometimes?

Step 5: Start Saving for Goals That Actually Excite You

Saving feels pointless if you don’t know why you’re doing it.

Popular Beginner Goals

- Vacation fund

- Home down payment

- New car

- Early retirement (yes, even beginners can think about this)

Label your savings accounts. “Emergency Fund” feels serious. “Italy Trip” feels motivating. Guess which one grows faster?

Pro tip: Automation changes everything. Set it once and let future-you say thanks.

Step 6: Investing Basics Without the Overwhelm

Investing scares beginners because nobody explains it simply. Let me fix that.

Investing means letting your money grow while you sleep. That’s the dream, right?

Beginner-Friendly Investing Options

- Employer 401(k), especially with matching

- Index funds

- Roth IRA

You don’t need to time the market or pick stocks like a movie genius. Start small. Stay consistent.

I delayed investing for years because I thought I needed “more money.” Turns out, time mattered way more.

Step 7: Protect Yourself With the Boring Stuff (Insurance Matters)

Insurance feels unexciting until you need it. Then it feels brilliant.

Key Types to Consider

- Health insurance

- Auto insurance

- Renters or homeowners insurance

- Life insurance (if others rely on your income)

Think of insurance as paying a small amount to avoid a massive disaster. Worth it.

Ever noticed how peace of mind feels priceless?

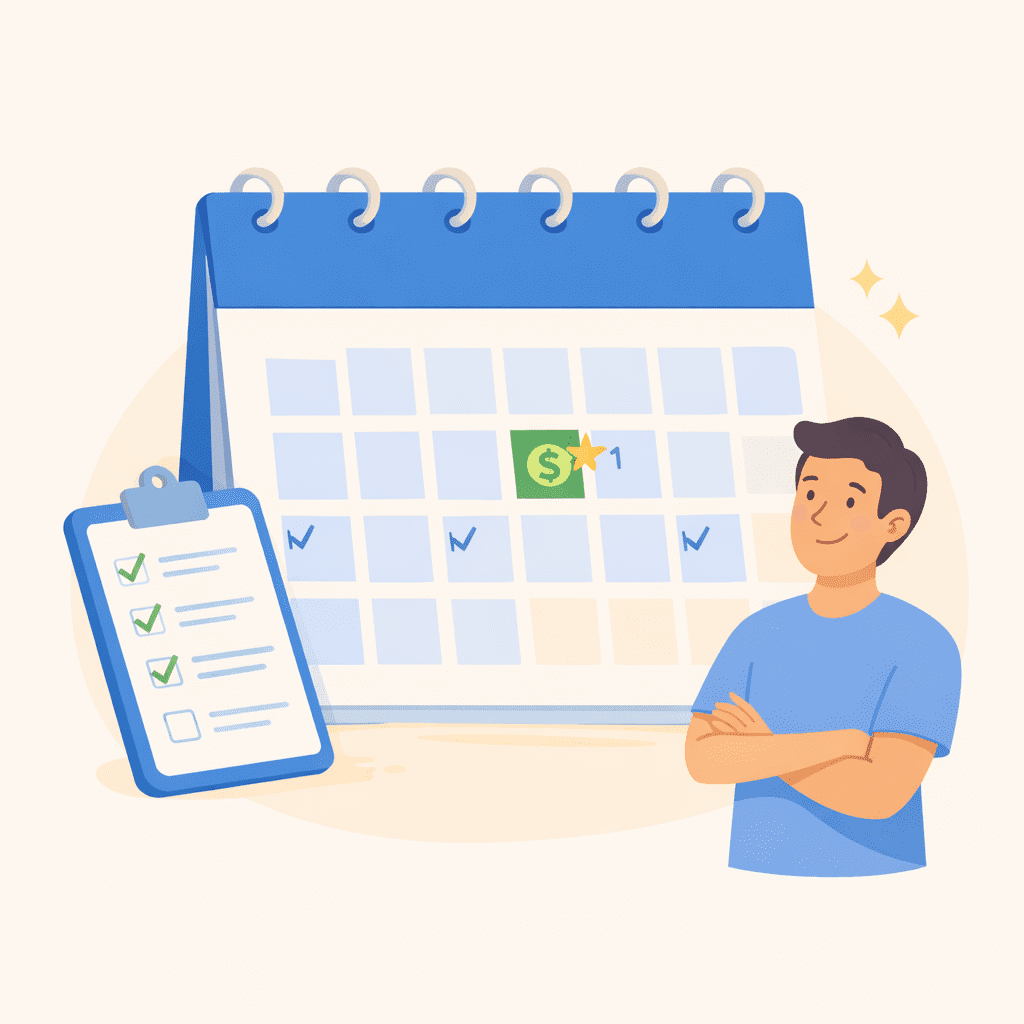

Step 8: Track Progress Without Obsessing

Financial planning for beginners works best when you check in—not hover.

Simple Monthly Check-In

- Review spending

- Adjust budget

- Celebrate wins (yes, even small ones)

I do a monthly “money date.” It takes 20 minutes and saves me weeks of stress later.

Avoid daily tracking if it stresses you out. Consistency beats intensity every time.

Common Myths That Need to Go (Right Now)

Let’s clear the nonsense.

- “I don’t make enough to plan.” Planning matters more when money feels tight.

- “I’ll start later.” Later costs more than starting now.

- “Financial planning is only for rich people.” Rich people got rich because they planned.

See the pattern?

How Financial Planning Actually Changes Your Life

This part surprised me the most.

Financial planning didn’t just improve my bank account. It:

- Reduced anxiety

- Improved decision-making

- Gave me confidence

- Helped me say “yes” without guilt

Money stopped controlling my mood. That alone felt worth the effort.

Ever wondered why confident people seem calmer? They usually have a plan.

Simple Tools That Make Everything Easier

You don’t need fancy software. Start simple.

Beginner Tools

- Budgeting apps

- Spreadsheets

- Automatic bank transfers

- Calendar reminders

Pick tools that fit your personality. If you hate spreadsheets, don’t force it.

Final Thoughts: Start Small, Start Now

Financial planning for beginners doesn’t demand perfection. It demands action.

You don’t need to master everything today. You just need to:

- Know your numbers

- Build a simple plan

- Stay consistent

Money gets way less scary when you stop avoiding it. Trust me—I tried avoidance. It sucked.

So take one step today. Open your bank app. Write one number down. Future-you will appreciate it more than you realize.

And hey, if you mess up? Welcome to being human. Just keep going 😉