Financial Planning Checklist You Can Follow

Let’s be real for a second. Most people don’t fail at money because they’re “bad with numbers.” They fail because they never had a clear financial planning checklist to follow in the first place. I’ve been there—spreadsheets half-made, budgets abandoned, and a vague hope that Future Me would magically figure things out. Spoiler alert: Future Me was annoyed.

So grab a coffee ☕, sit back, and let’s talk money like normal humans do. No lectures. No finance-bro nonsense. Just a practical, friendly checklist you can actually stick with.

Why You Need a Financial Planning Checklist (Yes, You Really Do)

Ever notice how people love setting goals but hate systems? That’s exactly why a financial planning checklist works so well. It removes decision fatigue and replaces it with clear next steps.

I don’t wake up every month wondering, “What should I do with my money?” I just follow the list. Simple beats fancy every time, IMO.

Here’s what a solid checklist does for you:

- Keeps you consistent, even when motivation disappears

- Stops impulsive money decisions (hello, random Amazon purchases)

- Turns big goals into small, doable actions

And honestly, who doesn’t want less stress and more control?

Step 1: Get Clear on Your Money Reality (No Judgment Allowed)

Know Your Monthly Income

Before planning anything, you need to know what actually hits your bank account. Not your salary on paper—your real take-home pay after taxes.

Include:

- Your main paycheck

- Side hustle income

- Freelance or contract work

- Any recurring income streams

Be honest here. Guessing only hurts future you.

Track Your Expenses Like a Detective

Yes, this part feels boring. Yes, it matters more than you think.

List everything:

- Rent or mortgage

- Utilities

- Groceries

- Subscriptions (yes, even that one you forgot about)

- Eating out and “fun money”

When I first did this, I realized my coffee habit deserved its own budget line. Painful? Slightly. Helpful? Absolutely.

Step 2: Set Clear Financial Goals (Not Vague Wishes)

Ever say, “I want to save more money” and then… not do that? Same. Goals need structure.

Short-Term Goals (0–2 Years)

These give you quick wins and motivation.

Examples:

- Build a $1,000 starter emergency fund

- Pay off one credit card

- Save for a vacation without using debt

Long-Term Goals (3+ Years)

This is where life stuff lives.

Examples:

- Retirement savings

- Buying a home

- Financial independence (aka not panicking over bills)

Write these down. Seriously. Your brain takes written goals more seriously.

Step 3: Create a Budget You Won’t Hate

Let’s kill a myth real quick. A budget doesn’t kill your freedom. A bad budget does.

Pick a Budgeting Style That Fits You

Different people need different systems. I’ve tried them all, and here’s the honest breakdown:

- 50/30/20 Rule – Great for beginners who want simplicity

- Zero-Based Budget – Perfect if you love control and details

- Pay Yourself First – Ideal if saving feels hard

The best budget is the one you actually use. Not the fanciest one on TikTok.

Build in Fun Money (Yes, Really)

If your budget doesn’t allow joy, it will fail. Period.

Add:

- Eating out

- Entertainment

- Hobbies

- Small guilt-free splurges 🙂

That $50 you plan beats the $300 you “accidentally” spend.

Step 4: Build Your Emergency Fund (Your Financial Seatbelt)

Life loves surprises. Your emergency fund protects you when things go sideways.

How Much Should You Save?

Start small. Momentum matters.

- $1,000 starter fund

- Then 3–6 months of essential expenses

Keep this money:

- In a high-yield savings account

- Separate from daily spending

- Easy to access, but not too easy

I once avoided a credit card spiral thanks to this fund. That alone sold me for life.

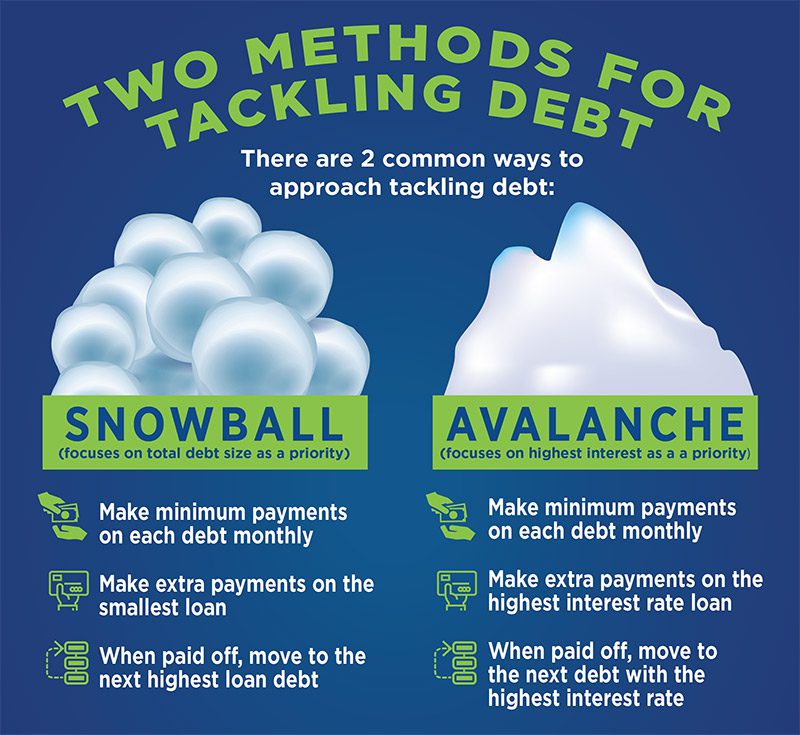

Step 5: Kill High-Interest Debt First (No Mercy)

Debt with high interest rates drains your future faster than anything else.

Prioritize These First

Focus on:

- Credit cards

- Payday loans

- High-interest personal loans

Two popular strategies work well:

- Debt Snowball – Small wins keep motivation high

- Debt Avalanche – Saves more on interest long-term

Pick one and commit. Half-debt strategies help no one.

Step 6: Protect Yourself With the Right Insurance

Insurance feels boring—until you need it. Then it feels brilliant.

Essential Coverage to Review

Make sure you have:

- Health insurance (non-negotiable in the US)

- Auto insurance with adequate liability

- Renter’s or homeowner’s insurance

- Life insurance if someone depends on your income

Think of insurance as paying a small amount to avoid financial disasters. Fair trade, right?

Step 7: Start Investing (Even If You Feel Late)

Let me say this clearly: You don’t need to be rich to invest.

Start Simple

Begin with:

- Employer-sponsored retirement plans (hello, 401(k) match)

- Roth IRA or Traditional IRA

- Low-cost index funds

Time matters more than perfection. Starting “late” still beats not starting at all.

Automate Everything

Automation turns good intentions into real progress.

Set up:

- Automatic contributions

- Automatic increases when income grows

- Automatic reinvestments

Future You will thank you. Probably quietly, but still.

Step 8: Plan for Big Life Expenses Before They Sneak Up

Big expenses don’t appear out of nowhere. We just pretend they will.

Common Big-Ticket Items

Plan ahead for:

- Weddings

- Kids

- Home repairs

- Car replacements

- Medical costs

Create sinking funds so these don’t wreck your budget. Small monthly contributions beat panic every time.

Step 9: Review and Adjust Your Plan Regularly

A financial planning checklist isn’t a “set it and forget it” thing.

Do Regular Money Check-Ins

I recommend:

- Monthly quick reviews (15 minutes max)

- Quarterly deeper reviews

- Annual goal resets

Ask yourself:

- What’s working?

- What feels stressful?

- What needs tweaking?

Life changes. Your plan should too.

Step 10: Build Better Money Habits (This Is the Secret Sauce)

Here’s the truth no one loves to hear. Habits matter more than hacks.

Small Habits That Add Up

Focus on:

- Tracking expenses weekly

- Reviewing accounts monthly

- Avoiding lifestyle inflation

- Spending intentionally, not emotionally

FYI, discipline beats motivation every single time.

Common Financial Planning Mistakes to Avoid

Let’s save you some frustration.

Avoid these classics:

- Waiting for the “perfect time”

- Overcomplicating your plan

- Ignoring retirement because it feels far away

- Comparing your progress to others

Everyone runs a different race. Stay in your lane.

Your Simple Financial Planning Checklist (Bookmark This)

Here’s your quick-reference version:

- Know your income and expenses

- Set short- and long-term goals

- Create a realistic budget

- Build an emergency fund

- Pay off high-interest debt

- Get proper insurance

- Start investing early

- Plan for big expenses

- Review your plan regularly

- Strengthen money habits

Print it. Save it. Actually use it.

Final Thoughts: Progress Beats Perfection Every Time

If you take one thing away from this, let it be this: you don’t need a perfect plan—you need a followable one. A solid financial planning checklist gives you direction, confidence, and fewer “oh no” moments with money.

Start messy. Start small. Just start.

And hey, if you mess up? Welcome to being human. Adjust, laugh it off, and keep going 😄