How to Build a Financial Plan on a Low Income

Let me guess—you want a financial plan, but your bank balance laughs every time you open your app. Been there. I built my first financial plan on a low income when my idea of “extra money” meant skipping guac, not buying stocks. And guess what? It worked. Not overnight, not magically, but it worked in a very real, very human way.

If you think financial planning only works for people with six-figure salaries and color-coded spreadsheets, stick with me. We’re about to prove that wrong—without the boring lecture 😌.

Why a Financial Plan Matters (Even When Money Is Tight)

Here’s the uncomfortable truth: low income makes financial planning more important, not less. When money feels scarce, every dollar needs a job. Otherwise, it disappears faster than snacks at a Super Bowl party.

I used to think, “What’s the point of planning if I barely earn anything?” That mindset kept me stuck. Once I flipped it, everything changed.

A solid financial plan low income folks can follow helps you:

- Reduce money stress (huge win)

- Avoid stupid debt mistakes

- Create stability, even on a small paycheck

- Build momentum, not just survive

Ever noticed how stress drops when you know where your money goes? Exactly.

Step 1: Get Real About Your Income (No Fantasy Numbers)

Know Your Actual Monthly Income

Start with the number that actually hits your bank account. Not your “good month.” Not your “hopefully soon” raise. I mean your real, consistent income.

If your income changes month to month, use your lowest average. IMO, pessimistic math saves future-you from panic.

Include:

- Take-home pay after taxes

- Side gigs (average them out)

- Government benefits or credits, if applicable

Clarity beats optimism every time.

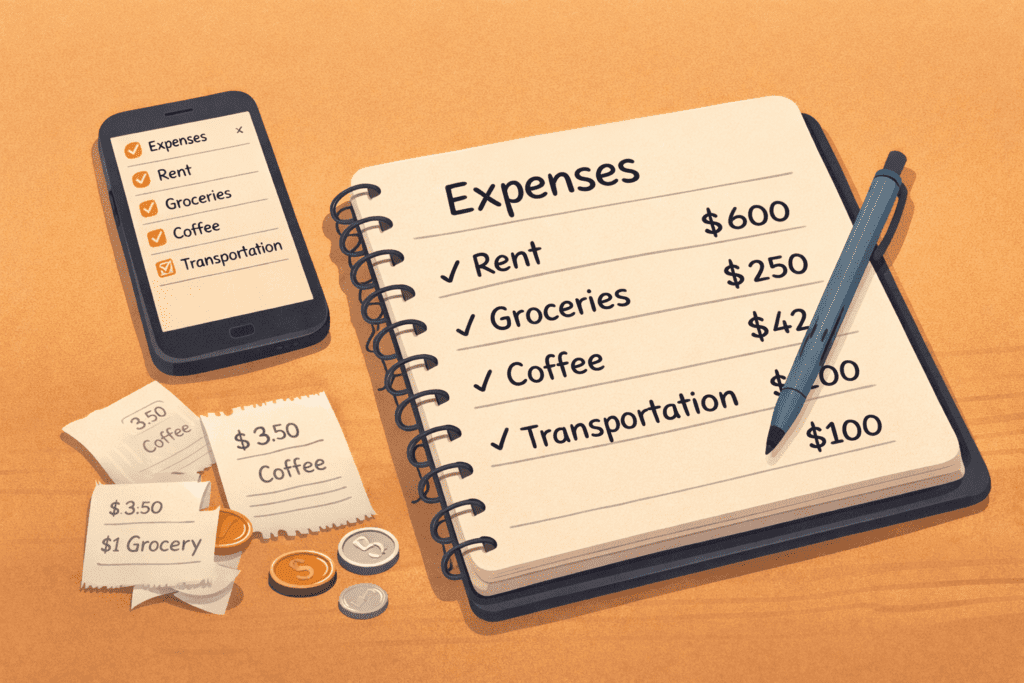

Step 2: Track Expenses Without Losing Your Mind

Yes, Tracking Matters (But Don’t Go Overboard)

You don’t need 12 apps and a finance degree. You need awareness.

I tracked my spending with:

- One notebook

- A notes app

- Mild judgment toward myself

That’s it.

Focus on:

- Rent

- Utilities

- Groceries

- Transportation

- Minimum debt payments

Then track the sneaky stuff. You know—the “just $8” purchases that somehow eat $200 a month.

Ask yourself: Do I control my money, or does my money freestyle?

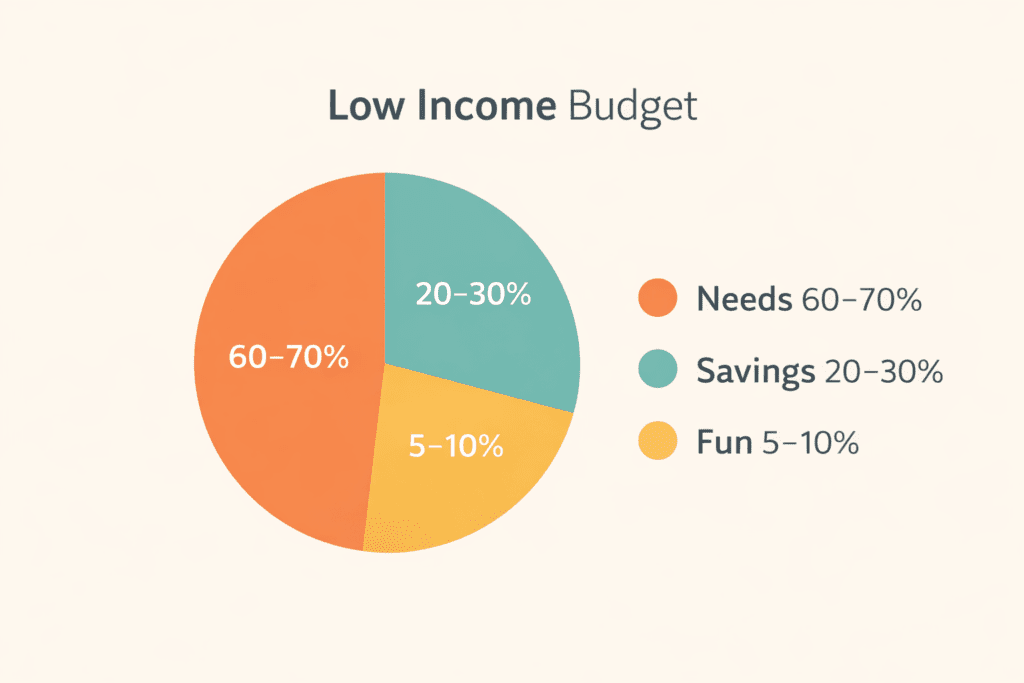

Step 3: Build a Bare-Bones Budget That Won’t Make You Quit

Forget Perfect Budgets—Aim for Livable Ones

A financial plan on a low income fails when it feels like punishment. I ditched strict budgets and built a flexible one instead.

Try this simple structure:

- Needs: 60–70%

- Financial goals: 20–30%

- Life/fun: 5–10%

Yes, even low income budgets need fun money. Otherwise, burnout shows up fast.

Budgets should support your life, not suffocate it.

Step 4: Start an Emergency Fund (Even If It’s $5)

Small Savings Still Count—Fight Me on This

I saved my first emergency fund in $10 chunks. No drama. No heroics. Just consistency.

Start with a tiny goal:

- $500 starter fund

- Then aim for 1 month of expenses

- Eventually build toward 3 months

Keep it:

- In a separate savings account

- Easy to access

- Not “accidentally spendable”

Ever had a flat tire turn into a financial meltdown? Yeah, emergency funds stop that nonsense.

Step 5: Tackle Debt Without Self-Hate

Low Income + Debt Needs Strategy, Not Shame

Debt feels heavier when income feels light. I focused on control, not speed.

Choose one method:

- Snowball: Smallest balance first for motivation

- Avalanche: Highest interest first to save money

Both work. Pick the one you’ll actually stick to.

Always pay minimums on everything. Then throw extra cash at one debt only. Even $20 counts.

FYI—ignoring debt doesn’t make it disappear. I tried. It did not work :/

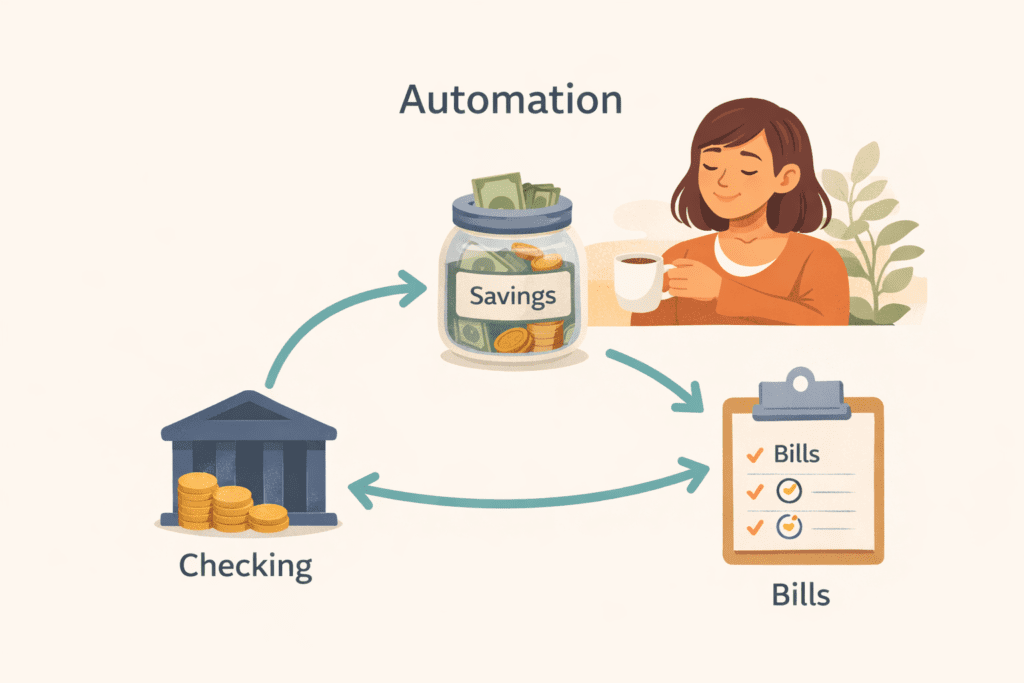

Step 6: Automate What You Can (Lazy Wins Here)

Automation Saves Willpower

When income feels tight, decision fatigue hits hard. Automation fixes that.

Set up:

- Automatic savings transfers (even $10)

- Auto-pay for bills

- Payment reminders if auto-pay scares you

I automated my savings and stopped “forgetting” to save. Funny how that works.

Low income planning works best when it runs in the background.

Step 7: Increase Income Without Burning Out

You Don’t Need a Hustle Empire

Yes, earning more helps. No, you don’t need three side hustles and zero sleep.

Start small:

- Ask for overtime

- Freelance one skill

- Sell unused stuff

- Pick short-term gigs

I boosted my income by tutoring two nights a week. Nothing glamorous. Just effective.

Ask yourself: What’s the least exhausting way I can earn a little more?

Step 8: Plan for the Future (Yes, Even Now)

Retirement Isn’t Only for Rich People

I avoided retirement planning for years because I felt “too broke.” Big mistake.

If your employer offers a 401(k) match:

- Contribute enough to get the match

- That’s free money—don’t leave it behind

If not:

- Open a Roth IRA

- Start with tiny contributions

Even $25 a month matters over time. Compound growth loves consistency, not income size.

Step 9: Set Financial Goals That Actually Motivate You

Vague Goals Kill Motivation

“Save more money” means nothing. I set goals that felt real.

Good goals sound like:

- “Save $1,000 by December”

- “Pay off one credit card this year”

- “Build one-month emergency fund”

Write them down. Track progress. Celebrate small wins.

Progress beats perfection every single time.

Step 10: Adjust, Don’t Quit

Your Plan Will Change—and That’s Normal

Life happens. Bills spike. Income dips. Motivation disappears.

That doesn’t mean your financial plan low income approach failed. It means you’re human.

When things change:

- Adjust numbers

- Lower goals temporarily

- Keep showing up

I revised my plan at least five times in one year. Each version worked better than the last.

Common Mistakes to Avoid on a Low Income Financial Plan

Let’s save you some pain.

Avoid these traps:

- Waiting to earn more before planning

- Cutting all joy from your budget

- Comparing yourself to higher earners

- Trying to be perfect instead of consistent

Perfection kills momentum. Consistency builds freedom.

What a Realistic Financial Plan on a Low Income Looks Like

Let me be blunt. A realistic plan looks:

- A little messy

- Slightly boring

- Very effective

It won’t turn you into a millionaire next year. It will give you control, confidence, and options.

And honestly? That’s priceless.

Final Thoughts: You’re Not Behind—You’re Building

If you take one thing from this, let it be this: you don’t need a high income to build a strong financial plan. You need intention, honesty, and patience.

Start small. Stay consistent. Adjust when life punches you in the face. It happens.

So, what’s your first move—tracking expenses or starting that emergency fund? Either way, you’re already ahead of where you were yesterday. And that’s a win worth celebrating 🙂