Debt Payoff Challenge That Actually Works

Debt sucks. But paying it off doesn’t have to. If you’re staring at your credit card statement like it’s a horror movie, a debt payoff challenge might be your ticket to financial freedom—or at least fewer sleepless nights. These challenges turn the boring grind of debt repayment into something almost fun. Almost. Let’s dive into the best ones to try.

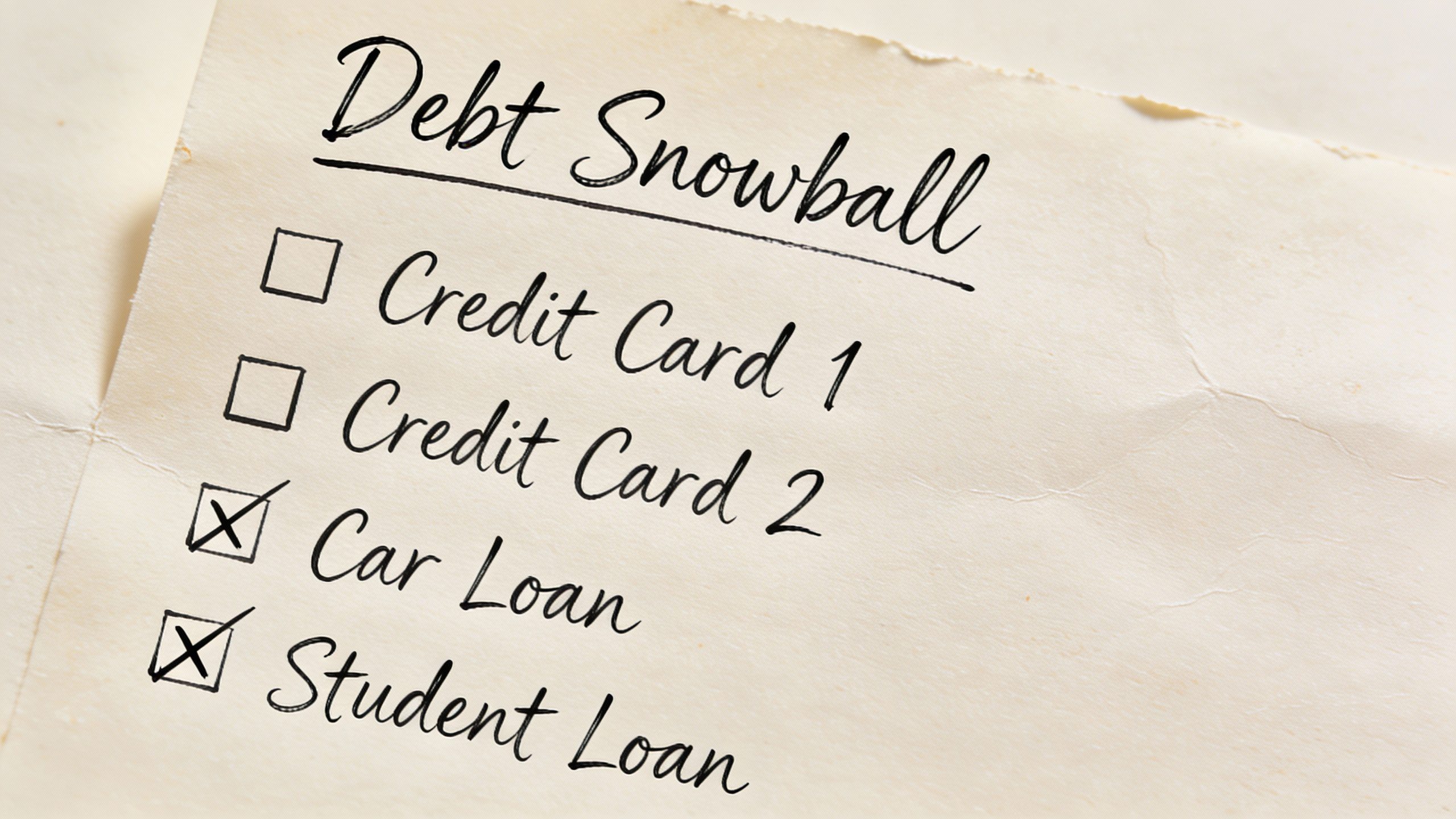

The Snowball Method: Start Small, Win Big

Made famous by Dave Ramsey, the Snowball Method is all about psychological wins. You list your debts from smallest to largest, attack the smallest balance first, and roll those payments into the next debt like an avalanche of financial badassery.

Why It Works

Humans need instant gratification. Paying off a $500 medical bill feels way more satisfying than chipping away at a $20K student loan. The momentum keeps you motivated.

How to Try It

- List all debts by balance (ignore interest rates).

- Pay minimums on everything except the smallest debt.

- Throw every extra dollar at Debt #1 until it’s gone.

- Repeat with the next smallest debt.

The Avalanche Method: For Math Nerds (and Penny-Pinchers)

If you’d rather save money than feel feelings, the Avalanche Method is your jam. You tackle debts with the highest interest rates first, saving you the most cash long-term.

Why It Works

Credit card companies hate this one simple trick! Seriously, you’ll pay less in interest—which means more money for, you know, things that don’t suck.

How to Try It

- List debts by interest rate (highest to lowest).

- Pay minimums on everything except the top offender.

- Crush the high-interest debt like it insulted your dog.

- Move down the list.

The No-Spend Challenge: Shock Your Wallet Into Submission

Ever notice how your bank account mysteriously empties after “just one” Target run? A no-spend challenge forces you to confront your spending habits—and your demons.

How to Survive

Pick a timeframe (a week, a month) and only spend on absolute essentials: rent, groceries, utilities. No lattes, no impulse buys, no “but it was on sale!” excuses.

Pro Tip

Use the money you save to bulldoze a debt. FYI, you’ll also discover how many things you “need” are actually just wants in disguise.

The 30-Day Debt Sprint

Think of this as a financial boot camp. For 30 days, you go all-in on cutting expenses and increasing income to throw as much cash as possible at debt.

- Sell stuff you don’t need (yes, even that collectible Funko Pop).

- Pick up a side hustle (dog walking, freelancing, selling dubious life advice on the internet).

- Slash subscriptions, dine-in like a monk, and embrace temporary frugality.

It’s intense, but the progress is addicting. IMO, it’s worth the short-term pain.

The Debt Snowflake Challenge: Small Change, Big Impact

Not ready for a full-blown sprint? Snowflaking is the art of throwing tiny amounts of money at your debt whenever you can. Found $5 in your jacket? Debt payment. Got a $10 rebate? Debt payment.

Why It’s Genius

Those “insignificant” amounts add up fast. Plus, it keeps you mentally engaged with your debt instead of ignoring it like an awkward text.

FAQ: Your Burning Debt Challenge Questions

Which Method Saves the Most Money?

The Avalanche Method, hands down. But if you need motivation more than math, Snowball might work better for you.

What If I Have Multiple Types of Debt?

Prioritize high-interest debt first (looking at you, credit cards). Student loans and mortgages can wait—they’re not actively bleeding your wallet dry.

Can I Combine Challenges?

Absolutely! Try a no-spend month while snowflaking, or use the 30-day sprint to kickstart your Snowball Method. Get creative.

How Do I Stay Motivated?

Track progress visually—a spreadsheet, a jar of marbles, a dramatic “DEBT FREE” countdown on your fridge. Celebrate small wins (just not by spending money).

What If I Slip Up?

Debt payoff isn’t linear. Forgive yourself and jump back in. One missed month doesn’t undo progress—quitting does.

Ready to Pick Your Fight?

Debt doesn’t disappear by magic (unless you win the lottery, and let’s be real—you won’t). But with the right challenge, you can turn the slog into a game you actually want to win. Pick a method, commit, and watch those balances shrink. Your future self will high-five you.