Debt Avalanche Method Explained for Beginners

Struggling with debt feels like carrying a backpack full of bricks—it slows you down, makes everything harder, and just plain sucks. But here’s the good news: you don’t have to keep lugging it around forever. The debt avalanche method is one of the smartest ways to crush your debt efficiently, and it’s not as complicated as it sounds. Let’s break it down so you can start ditching those payments like a pro.

What Is the Debt Avalanche Method?

Imagine you owe money on a bunch of different debts—credit cards, student loans, maybe a personal loan or two. The avalanche method is a strategy where you tackle your debts in a specific order to save the most money on interest over time.

Here’s how it works in a nutshell:

- List all your debts by interest rate—highest to lowest.

- Pay the minimum on everything except the debt with the highest rate.

- Throw every extra dollar you can at that top debt until it’s gone.

- Repeat the process with the next highest rate, and so on.

Unlike the “debt snowball” method (which focuses on paying off the smallest balances first), the avalanche is all about math, not motivation. It’s the financially optimal way to eliminate debt—but that doesn’t mean it’s always easy.

Why It Works (The Nerdy Math Part)

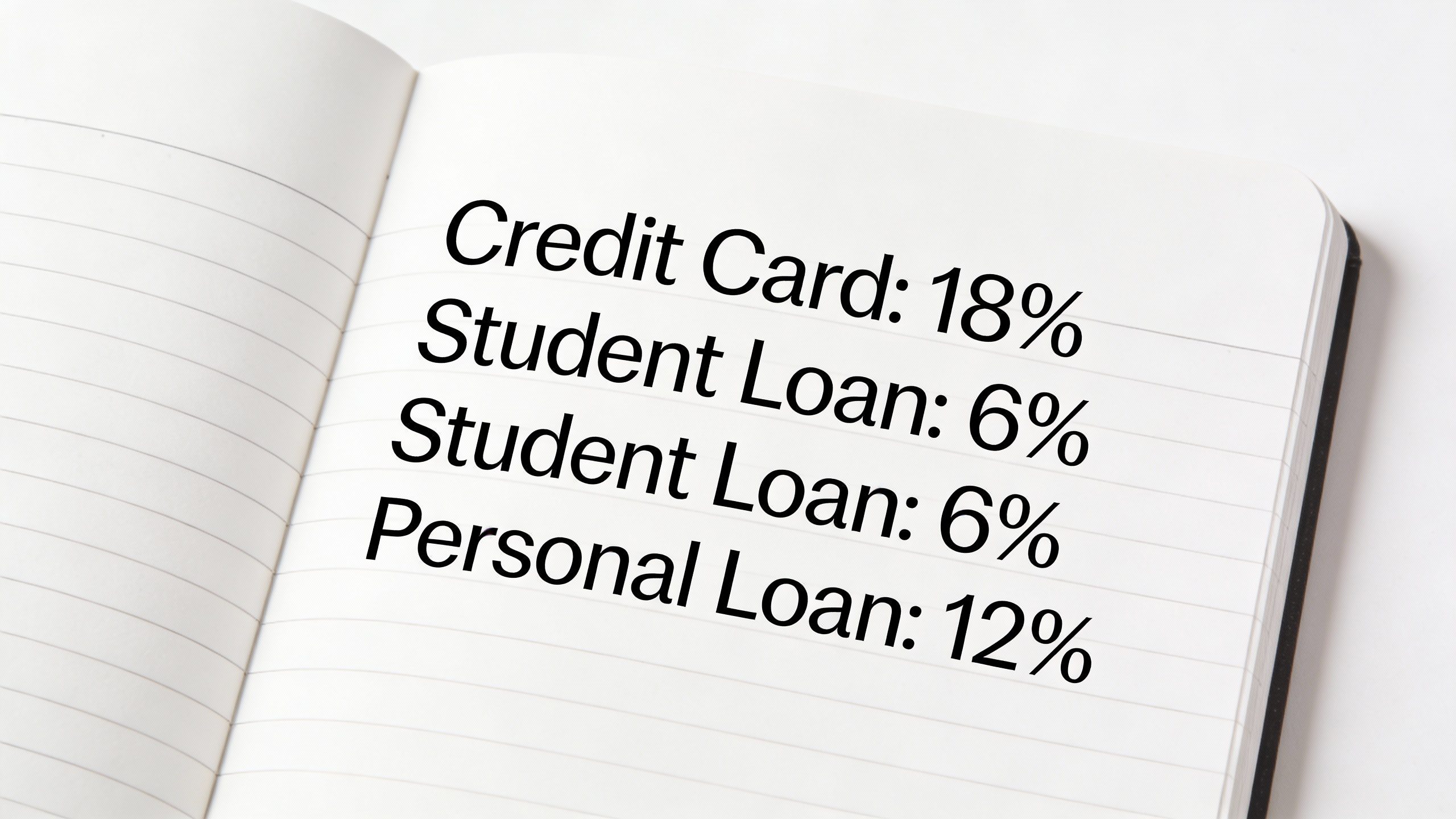

High-interest debt grows faster than low-interest debt. A credit card at 24% APR costs you way more over time than a student loan at 6%. By targeting the most expensive debt first, you stop the bleeding where it hurts the most.

Think of it like plugging leaks in a sinking boat. You’d patch the biggest hole first, right? Same logic applies here.

Debt Avalanche vs. Snowball: Which Is Better?

This is the personal finance version of “Pepsi vs. Coke.” Both methods work, but they appeal to different people.

- Debt Avalanche: Saves you more money in interest. Best for people who are motivated by efficiency and don’t mind delayed gratification.

- Debt Snowball: Pays off smaller balances first for quick wins. Better for folks who need psychological boosts to stay on track.

IMO, if you can stick with it, the avalanche is the smarter play. But hey, if you need those quick wins to avoid quitting, the snowball isn’t a bad choice either. The best method is the one you’ll actually *do*.

Step-by-Step: How to Use the Debt Avalanche Method

Ready to put this into action? Here’s your game plan:

1. List All Your Debts (Yes, All of Them)

Grab a spreadsheet, notebook, or even a napkin—whatever works. Write down:

- Debt name (e.g., “Chase Credit Card”)

- Current balance

- Interest rate (APR)

- Minimum payment

Sort them by interest rate, highest to lowest. No cheating—this isn’t the time to ignore that 29% APR store card you opened for a 10% discount.

2. Budget for Minimum Payments

Pay the minimum on every debt to avoid penalties. Then, any extra money you can scrape together (from cutting expenses, side hustles, or selling your collection of questionable eBay purchases) goes toward the top debt on your list.

3. Attack the Highest-Interest Debt Relentlessly

This is where the magic happens. Every extra dollar you throw at that top debt shortens its lifespan and saves you cash. Once it’s gone, take the money you were putting toward it and roll it into the next debt on your list.

Common Mistakes to Avoid

Even the best plans can derail if you’re not careful. Here’s what trips people up:

- Not tracking progress: Use an app or spreadsheet to see your debts shrinking. Visual wins keep you motivated.

- Skipping the budget: If you don’t know where your money’s going, you can’t free up extra cash to throw at debt.

- Taking on new debt: Put the credit cards on ice (literally—try freezing them in a block of water if you’re tempted).

FYI, this isn’t a “set it and forget it” strategy. You’ve gotta stay engaged and adjust as needed.

When the Debt Avalanche Might NOT Be the Best Fit

The avalanche method isn’t perfect for everyone. Here’s when you might want to reconsider:

- You’re drowning in small debts: If you have 10 tiny balances, the snowball method’s quick wins might keep you from giving up.

- Your highest-interest debt is massive: If your #1 debt is a $50K loan, it might take forever to knock out. Some people need quicker momentum.

- You’re dealing with emotional burnout: Personal finance is as much about behavior as math. If avalanche feels soul-crushing, switch tactics.

FAQ: Your Debt Avalanche Questions, Answered

Does the debt avalanche method hurt your credit score?

Nope! Paying down debt usually helps your credit over time. Just keep making minimum payments on everything to avoid late marks.

How long does it take to see results?

Depends on your debt load and how much extra you can pay. The first one might take months, but each debt after that gets easier.

What if I can’t afford extra payments?

Then the avalanche (or any method) won’t work. Focus on increasing income or cutting expenses first. Even an extra $20/month helps.

Should I consolidate my debts to use this method?

Only if you get a lower interest rate. Consolidating high-interest debt into a lower-rate loan can turbocharge your avalanche plan.

Can I use this with credit card balance transfers?

Absolutely! Transfer high-interest balances to a 0% APR card, then avalanche the rest. Just don’t rack up new debt on the old cards.

Is this method only for credit cards?

Nope—it works for any debt with interest: student loans, personal loans, car payments, etc. If it charges interest, it’s fair game.

Final Thoughts: Is the Debt Avalanche Right for You?

The debt avalanche isn’t flashy, but it’s ruthlessly effective. If you’re the type who gets a weird thrill from optimizing spreadsheets (no judgment), this method will feel like a superhero power.

But remember: The best debt payoff strategy is the one you stick with. Whether you choose avalanche, snowball, or some hybrid approach, the goal is the same—getting rid of debt for good. Now go forth and crush those balances!