How to Create a Financial Plan Step by Step

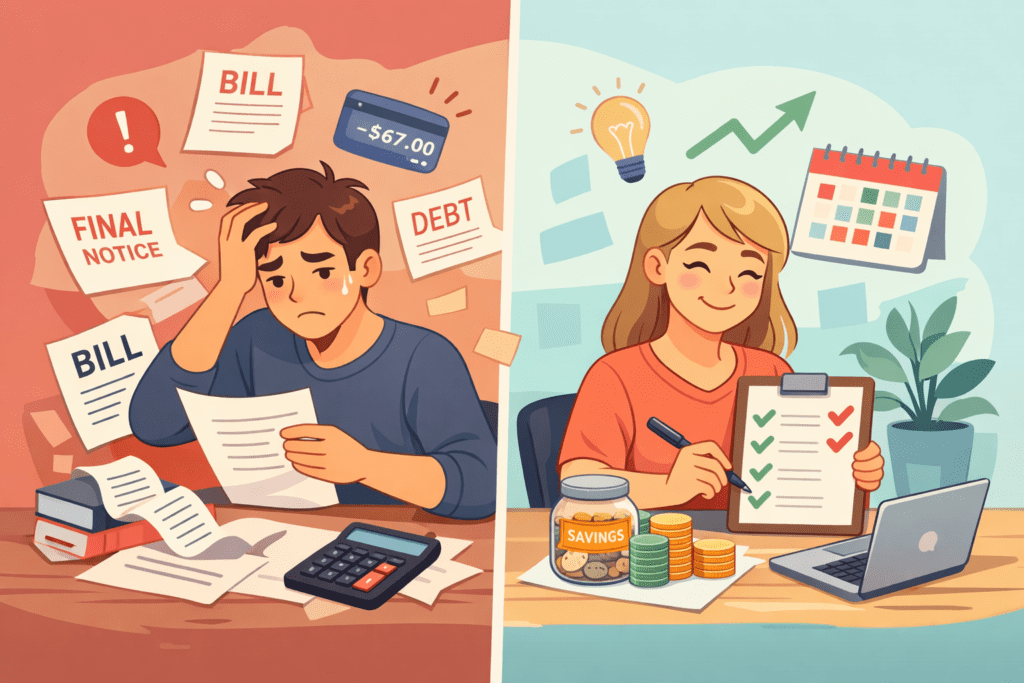

Money stress has a funny way of showing up uninvited. One minute you feel fine, and the next you panic over a credit card notification like it’s a horror movie jump scare. 😅 I’ve been there, and that’s exactly why I learned how to create a financial plan step by step instead of just “hoping things work out.”

Let’s keep this simple, practical, and human. No finance-bro jargon. No lectures. Just a real conversation about how to get your money under control without losing your mind.

Why You Even Need a Financial Plan (Yes, You Do)

Ever wondered why some people seem calm about money while others freak out every payday? It’s not luck. It’s clarity.

A financial plan gives you:

- Direction for your money instead of random spending

- Confidence when bills pop up

- Freedom to enjoy life without guilt

IMO, a financial plan doesn’t restrict you. It actually gives you permission to spend without stress.

Step 1: Get Real About Your Current Money Situation

Before you plan anything, you need to face reality. No judgment. No shame. Just facts.

Check Your Income

Write down every dollar coming in each month:

- Salary (after tax, not the fantasy number)

- Side hustles

- Freelance income

- Anything else that hits your bank account

This number becomes your foundation. Everything else depends on it.

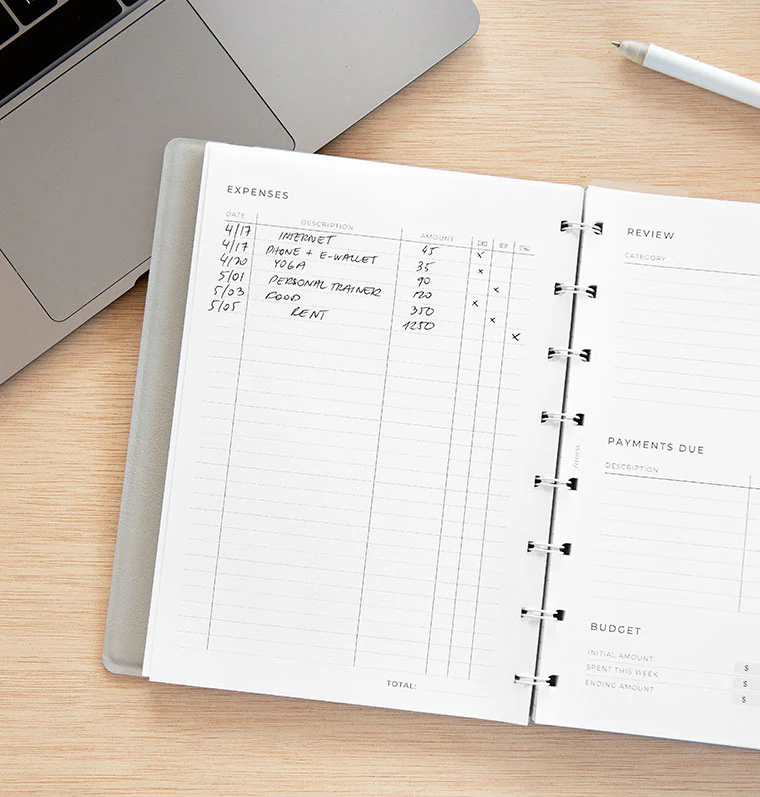

Track Your Expenses (Yes, All of Them)

This part feels annoying, but it works.

List:

- Rent or mortgage

- Utilities

- Groceries

- Subscriptions (looking at you, forgotten streaming apps)

- Fun spending

FYI: Most people underestimate their expenses. Don’t be that person.

Step 2: Define Clear Financial Goals (No Vague Wishes)

“I want to be rich” doesn’t count as a goal. Sorry.

Short-Term Goals (0–2 Years)

These keep you motivated fast:

- Build a $1,000 emergency fund

- Pay off a credit card

- Save for a vacation

Medium-Term Goals (3–5 Years)

These need consistency:

- Buy a car

- Save for a home down payment

- Start investing seriously

Long-Term Goals (10+ Years)

These shape your future:

- Retirement

- Financial independence

- Legacy planning

Bold truth: Goals give your financial plan meaning. Without them, budgeting feels pointless.

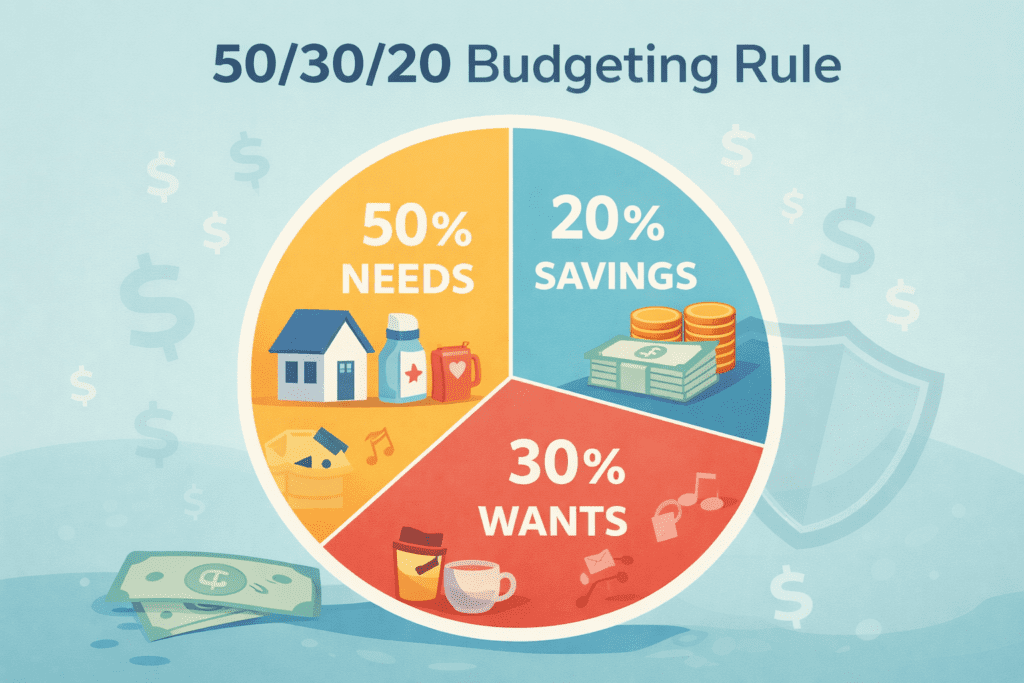

Step 3: Build a Budget That Doesn’t Make You Miserable

Let’s talk budgeting without the suffering.

Use a Simple Budgeting Framework

I personally like the 50/30/20 rule because it doesn’t overcomplicate life.

- 50% Needs: rent, food, bills

- 30% Wants: dining out, hobbies, fun

- 20% Savings & debt payoff

Does it need tweaking? Sure. But it’s a solid starting point.

Automate What You Can

Automation saves you from yourself.

- Auto-transfer savings

- Auto-pay bills

- Auto-invest contributions

When money moves automatically, you stop relying on motivation (which disappears fast).

Step 4: Build an Emergency Fund (Because Life Happens)

Ever had your car break down right after you felt “financially okay”? Same.

How Much Should You Save?

Start small:

- $500

- Then $1,000

- Eventually 3–6 months of expenses

Keep this money:

- In a high-yield savings account

- Easily accessible

- Separate from spending money

Key rule: This fund exists for emergencies, not sales at Target.

Step 5: Eliminate High-Interest Debt Like a Pro

Debt steals your future paycheck. Dramatic? Yes. True? Also yes.

Focus on High-Interest Debt First

Target:

- Credit cards

- Payday loans

- High-interest personal loans

Two popular strategies:

- Avalanche method: highest interest first

- Snowball method: smallest balance first

I prefer avalanche because math wins, but snowball feels better emotionally. Pick what keeps you consistent.

Step 6: Start Investing (Even If You Feel Late)

If you think you’re “too late,” welcome to the club. Start anyway.

Keep It Simple at First

You don’t need fancy strategies.

- Employer 401(k) with match? Use it.

- Roth IRA? Solid option.

- Low-cost index funds? Chef’s kiss.

Bold reminder: Time in the market beats timing the market. Always.

Invest Consistently

Set monthly contributions and forget about them. Market ups and downs feel scary, but consistency wins long-term.

Step 7: Protect Your Plan With Insurance

Insurance feels boring until you need it.

Must-Have Coverage

- Health insurance

- Auto insurance

- Renters or homeowners insurance

- Life insurance (if others depend on you)

This step protects everything you’re building. Skip it, and one bad event can wreck years of progress.

Step 8: Plan for Retirement Like Your Future Self Depends on It

Because… they do.

Know Your Retirement Number

Ask yourself:

- When do I want to retire?

- What lifestyle do I want?

- How much will that cost per year?

Then work backward. Retirement planning feels less scary when you turn it into math instead of mystery.

Step 9: Review and Adjust Your Financial Plan Regularly

Your life changes. Your plan should too.

When to Review Your Plan

- New job

- Pay raise

- Big expense

- Once every 6–12 months minimum

Ask yourself:

- Does this still fit my goals?

- Can I save more?

- Am I happier with my money choices?

This step keeps your financial plan alive, not outdated.

Common Mistakes to Avoid When You Create a Financial Plan Step by Step

Let’s save you some pain.

- Trying to be perfect from day one

- Ignoring small expenses (they add up fast)

- Not adjusting your plan when life changes

- Comparing your journey to someone else’s highlight reel

Money progress isn’t linear. Expect bumps.

How Long Does It Take to See Results?

Short answer: faster than you think.

- Clarity: immediate

- Stress reduction: within weeks

- Real progress: a few months

- Life-changing results: years

Stick with it. Small steps compound like crazy.

Final Thoughts: Your Financial Plan Is Your Power Move

Creating a financial plan step by step changed how I think about money. I stopped guessing. I stopped stressing. I started choosing.

You don’t need perfection. You need clarity, consistency, and patience. Start messy. Adjust often. Keep going.

So… what’s the first step you’ll take today? Even one small move puts you ahead of yesterday. And trust me, future-you will absolutely thank you for it. 🙂