How to Change Your Money Thinking for Long-Term Wealth

Money doesn’t have to be boring, stressful, or something you avoid thinking about. In fact, the way most people approach money is completely backward—focusing on scarcity instead of possibility, restriction instead of freedom. What if you could flip that script? Let’s talk about how to think differently about money, not just as a tool for survival, but as a tool for building the life you actually want.

Money Isn’t Good or Evil—It’s Just a Tool

We love to moralize money. “Rich people are greedy!” “Money corrupts!” But here’s the thing: money is neutral. It’s like a hammer—you can use it to build a house or smash your thumb. The difference lies in how you wield it.

Instead of treating money like some mystical force, think of it as leverage. It buys you time, options, and yes, even peace of mind. The sooner you detach emotional baggage from it, the better decisions you’ll make.

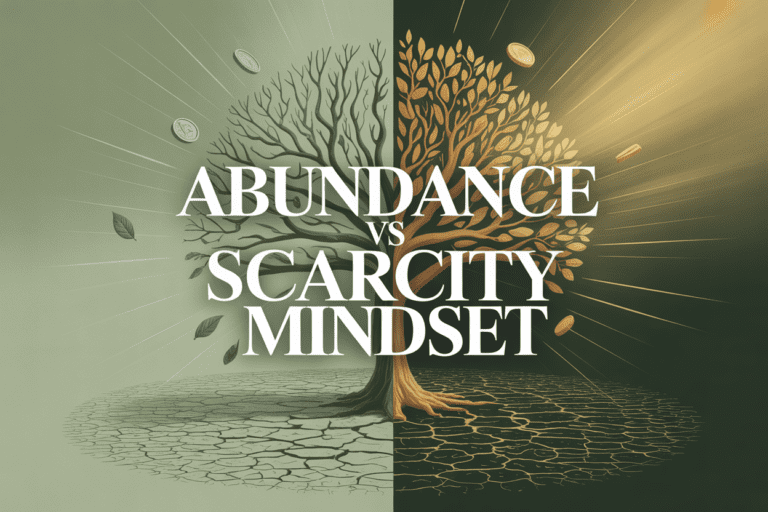

The Scarcity Mindset Trap

Most of us grew up hearing things like, “Money doesn’t grow on trees!” or “We can’t afford that.” Those statements wire your brain to see money as finite, which leads to fear-driven choices.

But what if you shifted to an abundance mindset? That doesn’t mean ignoring reality—it means focusing on opportunities instead of limitations. Instead of asking, “Can I afford this?” ask, “How can I afford this?”

Stop Budgeting Like a Prison Warden

Budgets get a bad rap because most people treat them like punishment. “No more avocado toast for you!” But a budget shouldn’t feel restrictive—it should feel empowering.

Think of it as a spending plan, not a deprivation plan. Allocate money for what you truly value (travel, hobbies, whatever lights you up) and cut the BS expenses that don’t.

The 50/30/20 Rule (But Make It Flexible)

The classic budgeting rule is:

- 50% needs (rent, groceries, bills)

- 30% wants (dining out, hobbies)

- 20% savings/debt payoff

But here’s the kicker: if you hate rules, tweak it! Maybe you’re a minimalist who spends 40% on needs and puts 30% toward travel. Your money, your priorities.

Investing Isn’t Just for Rich People

The biggest myth? That investing is some elite club for Wall Street bros. Nope. Thanks to apps and fractional shares, you can start with $5.

The real magic of investing? Compound interest. It’s like planting a money tree that grows while you sleep. Even small, consistent contributions add up over time.

Where to Start (Without Overcomplicating It)

- Index funds or ETFs: Low-cost, diversified, and hands-off.

- Retirement accounts: 401(k), IRA—anything with tax perks.

- Automate it: Set up recurring transfers so you don’t have to think.

FYI, you don’t need to “pick stocks” to be an investor. Keep it simple.

Debt Doesn’t Have to Be a Life Sentence

Debt feels like a dark cloud hanging over your head, but not all debt is created equal. A mortgage at 3%? Not terrible. Credit card debt at 24%? Yikes.

Instead of panicking, attack high-interest debt first (the “avalanche method”) or knock out small balances for quick wins (the “snowball method”). Either way, progress beats perfection.

The Emotional Side of Debt

Debt shame is real, but guilt won’t pay your bills. Forgive past financial missteps and focus on what you can control now. Every extra payment is a step toward freedom.

Money Should Buy Freedom, Not Just Stuff

The goal isn’t to hoard cash like a dragon guarding gold. It’s to use money to design a life with more choices.

Ask yourself:

- What does “enough” look like for me?

- What would I do if money weren’t a concern?

- How can I align my spending with my values?

IMO, the best investment is the one that buys back your time—whether that’s retiring early, working remotely, or just stressing less.

FAQs: Quick Answers to Common Money Questions

How much should I save before investing?

Aim for a 3–6 month emergency fund first. You don’t want to sell investments in a panic because your car broke down.

Is it okay to spend money on fun things?

Absolutely! Deprivation leads to binge spending. Budget for guilt-free fun—it keeps you sane.

Should I pay off debt or invest?

If your debt’s interest rate is higher than potential investment returns (e.g., credit cards), pay the debt first.

How do I stop impulse spending?

Implement a 24-hour rule for non-essentials. Sleep on it—most “must-haves” lose their appeal fast.

What’s the easiest way to track spending?

Use an app like Mint or YNAB. Or, if you’re old-school, a spreadsheet. Just pick one and stick with it.

Can I negotiate bills?

Hell yes. Call your internet/cable/phone provider and ask for a better rate. The worst they can say is no.

Rethink Money, Rewrite Your Story

Money isn’t the enemy—nor is it the ultimate goal. It’s fuel for the life you want. Whether that means financial independence, more travel, or just sleeping better at night, thinking differently about money starts with questioning the defaults.

So, what’s one small money habit you can change today? (And no, “winning the lottery” doesn’t count.)