Budgeting Tips to Stop Overspending: Real-Life Wins

I’m not here to scold you about your spending. I’m here to help you shut down overspending with doable, real-life moves. You’ll stop creeping into the red and start protecting the stuff that actually matters—like a vacation fund, a new laptop, or just not stressing over groceries at 11 p.m. FYI, you’ve got this.

Know where the money actually goes

We start with a map, not a mystery. If you don’t know your numbers, you’re flying blind.

– Track for 30 days: every coffee, every impulse buy, every snack run. You’ll spot the real culprits.

– Categorize like a boss: needs (rent, utilities, groceries), nice-to-haves (restaurants, streaming), and could-live-without (that gadget you forgot you owned).

– Use a simple tool: a notebook, a spreadsheet, or a budgeting app. Pick one you won’t abandon in a week.

- List your fixed costs (rent, insurance, debt payments).

- Estimate variable costs (groceries, fuel, utilities).

- Forecast for the month and compare weekly.

Make a budget that actually sticks

Budgets aren’t a punishment; they’re a plan with room for life. Here’s how to make one you’ll actually follow.

– Give every dollar a job: you should know exactly where each dollar is going before the month starts.

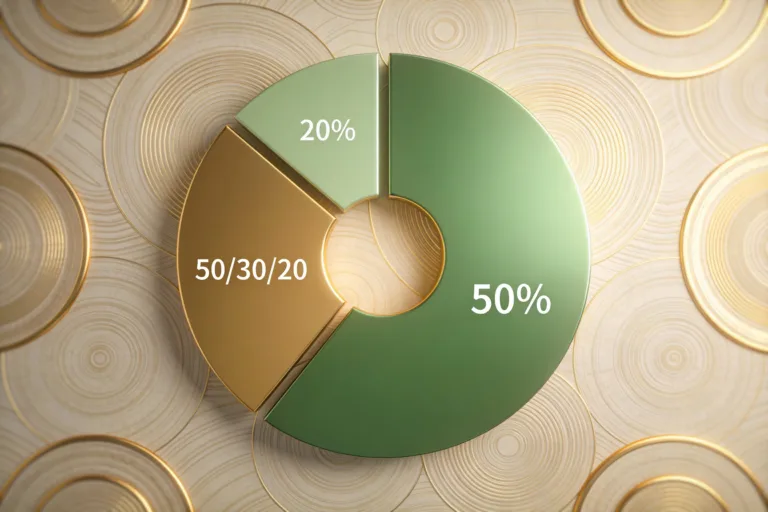

– Use the 50/30/20-ish framework, but tailor it: 50% needs, 30% wants, 20% savings/debt payoff. If you live in a high-cost area, bump needs a bit and trim wants.

– Build in a fun fund: a small separate pot for spontaneous joy. You’ll crave it less if you know you can still treat yourself.

Slay the impulse monster with practical triggers

Impulses strike fast. You can’t outmuscle them with willpower alone—you need triggers.

– Wait 24 hours for non-urgent purchases: you’ll usually forget about most of them or decide you didn’t need them.

– Limit “shopping moments”: set a timer before you browse online stores and only shop with a list.

– Unsubscribe from tempting emails and push notifications. If a deal looks too good to be true, it probably is.

– Flip the script: if you’re craving a debt-accumulator, channel that energy into a 15-minute decluttering sprint or a quick workout.

Automate the boring stuff

Automations save brainpower and keep you honest.

– Automate savings first: transfer a predefined amount to a savings account on payday.

– Automate debt payments: set up minimums plus a small extra if possible.

– Automate bill payments to avoid late fees. Late fees are stealthy budget assassins.

Smart shopping that actually saves you money

Saving doesn’t have to feel like deprivation. It can feel like a clever game you’re winning.

– Price check before big buys: use a quick search to compare prices and read reviews.

– Buy in bulk only for things you actually use and won’t spoil. Don’t fall for the “unit price” trap if you won’t finish it.

– Consider alternatives: store brands, coupons, or refurb items for tech.

– Set a “cool-down” period for non-essential purchases, like a 3-day rule for big-ticket items.

Debt and credit: treat them like plant care

If debt is a weed in your garden, you want to pull it out methodically.

– List all debts, interest rates, minimum payments. Tackle the high-interest stuff first if you can.

– Snowball or avalanche: pick a method that fits your personality. Snowball gives quick wins; avalanche saves more interest.

– Keep a no-new-debt pledge for a set period. Maybe 6 months or a year. FYI, this helps reset habits.

Protect your money with goals and accountability

Goals keep your budget from feeling like a chore.

– Set concrete, time-bound goals: pay off $3,000 of debt in 12 months, save $1,000 for emergencies this quarter, etc.

– Visualize progress: a simple chart or app that shows debt shrinking or savings growing is incredibly motivating.

– Find an accountability buddy: a friend, partner, or buddy from an online community. Check in weekly, no judgment.

H3: Tiny shifts that add up

Small changes compound fast when you stay consistent.

– Brew your coffee at home at least 5 days a week. Save the takeaway for special days.

– Pack lunches. It’s not glamorous, but it’s predictable.

– Review subscriptions quarterly: cancel the ones you barely use. That one streaming service you forgot you had? It’s stealing your future self’s lunch money.

H3: If you’re a spender who hates budgets

Budgets don’t have to feel like a prison sentence.

– Try a “zero-based” feel with a cushion: give every dollar a purpose, but leave a small cushion for tiny splurges.

– Swap fear-based budgeting for curiosity: ask what the money is enabling you to do in 6 months.

– Make it a game: reward yourself for meeting milestones with something small but meaningful.

H3: Emergency fund as your budget’s safety net

An emergency fund keeps you from swiping wildly when life happens.

– Start with a small target: $500 to $1,000 to cover small emergencies.

– Move toward 3-6 months of expenses as a bigger cushion.

– Keep it accessible but separate from everyday spending. A dedicated savings account helps.

FAQ

What’s the first step to stop overspending?

Start by tracking every dollar for 30 days. You’ll spot patterns, spends, and the real culprits behind the leaks. Then craft a simple budget that assigns every dollar a job. From there, automate savings and use a “cool-down” period for non-urgent buys.

Is it okay to use cash instead of cards?

Cash can be a powerful discipline tool because it makes the spending feel tangible. Try a weekly cash envelope for discretionary categories. When the cash is gone, you pause. If you hate carrying cash, use a debit card with strict daily limits or a budgeting app that tracks in real time.

How do I handle sudden expensive surprises?

Have an emergency fund and a plan: if something pops up, you don’t raid the debt pile. Use the fund for true emergencies, then rebuild it. If you don’t have a fund yet, borrow smartly (like 0% APR promos) only after you’ve cut a few non-essentials and reworked your budget.

What if my partner/spouse spends differently?

Open, honest conversations help. Create a joint budget that accounts for both incomes and align on non-negotiables. Agree on a shared “fun fund” for perks you both enjoy. Regular check-ins keep it from spiraling.

How long does it take to see real changes?

Most people notice smaller wins within a few weeks—the thrill of paying off a card, the joy of saving a few hundred dollars. Bigger shifts—like paying off a major debt or building a solid emergency fund—take a few months to a year. Stay consistent, and celebrate the milestones.

Conclusion

You don’t need a perfect plan to get control, you need a doable plan. Track your spending, build a budget that respects your life, automate what you can, and keep a little fun fund so you don’t feel denied. Budgeting is a tool, not a punishment—think of it as your financial sidekick helping you reach the things that actually matter. With a bit of persistence and a dash of humor, overspending loses its grip. You’ve got this, one mindful decision at a time.