Best Budgeting Methods for Beginners

Money keeps slipping through your fingers? You’re not broken—your budget is. The good news: you don’t need a finance degree or monk-like discipline to fix it. A few simple methods will help you understand where your money goes and make it go where you actually want. Pick one, tweak it, and watch the chaos calm down.

Start Here: Know Your Numbers

You can’t budget if you don’t know what you’re working with. Take 30 minutes, grab your bank app, and write down your net income and average monthly expenses. Yes, all of them—rent, groceries, coffee, streaming, random Amazon adventures.

- Income: Your take-home pay after taxes, plus side gigs.

- Fixed expenses: Rent, insurance, minimum debt payments, subscriptions.

- Variable expenses: Food, gas, fun, everything that wobbles.

- Savings/debt goals: Emergency fund, travel, extra debt payments.

You’ll probably find a few surprises. That’s normal. FYI, you’re not budgeting yet—you’re diagnosing.

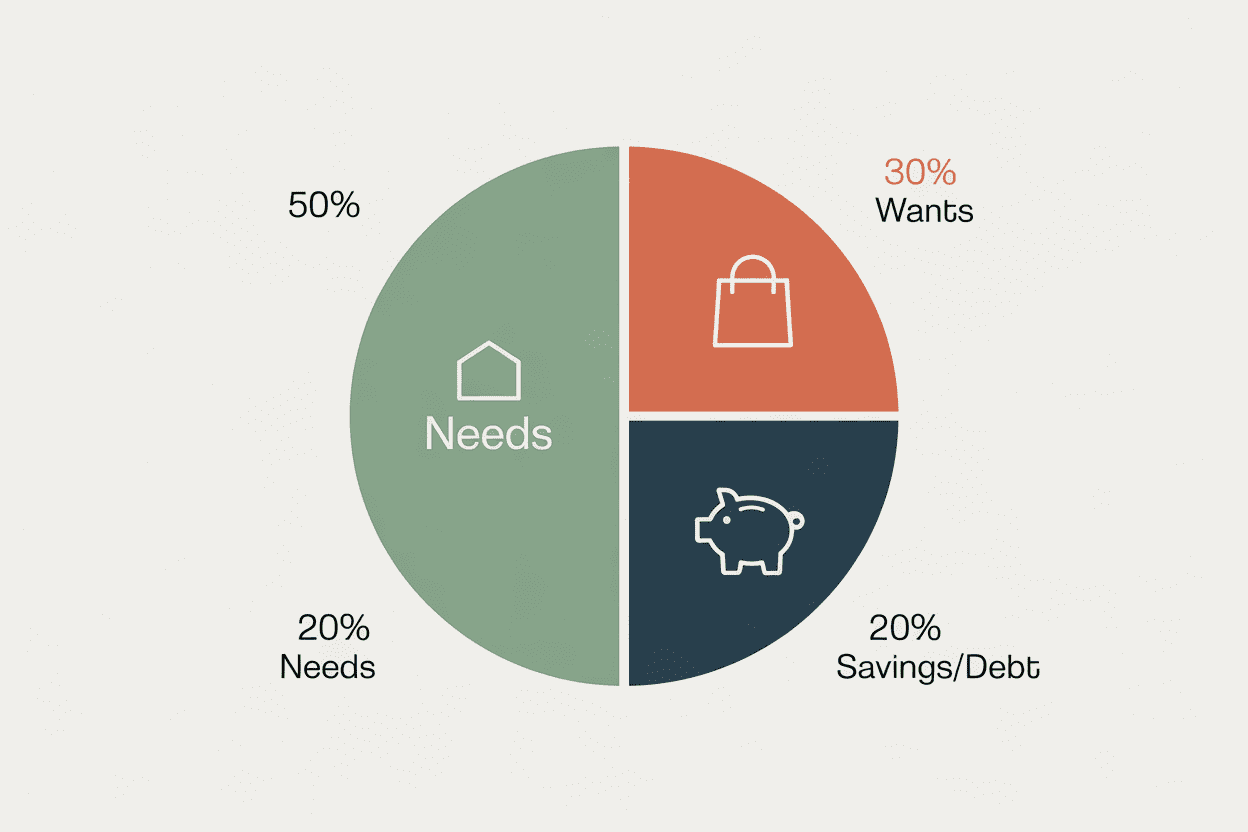

The 50/30/20 Rule: Clean and Simple

If you want a low-maintenance budget that still works, try the 50/30/20 rule. You split your net income into three buckets:

- 50% Needs: Housing, utilities, groceries, transportation, minimum debt payments.

- 30% Wants: Dining out, hobbies, travel, nicer-but-not-necessary upgrades.

- 20% Savings/Debt: Emergency fund, investments, extra debt payments.

This method keeps you honest without micromanaging every latte. If your “needs” exceed 50%, don’t panic—use it as a red flag to adjust over time.

When 50/30/20 Works Best

It shines when your expenses stay relatively steady and you want flexibility. You’ll still choose priorities, but you won’t obsess over line items.

Quick Tip: Automate It

Set up automatic transfers: savings on payday, then bills, then live off the rest. If you never see the money, you won’t miss it.

Zero-Based Budgeting: Give Every Dollar a Job

Zero-based budgeting takes the opposite approach. You assign every single dollar a purpose—spending, saving, or debt—until your income minus expenses equals zero. No, you don’t empty your bank account. You just stop leaving money unassigned.

- Pros: Crystal-clear control, great for digging out of debt or hitting big goals fast.

- Cons: Requires weekly check-ins. If you hate details, you might resist.

How to Set It Up

- List your income for the month (be conservative if it fluctuates).

- Budget for fixed bills first.

- Add categories for variable spending and savings goals.

- Adjust until every dollar has a job. Buffer category highly recommended.

IMO, this method builds the strongest money awareness. It’s like turning on the lights in a messy room—annoying at first, then weirdly satisfying.

Pay Yourself First: The Minimalist Favorite

Hate categories? Pay yourself first and let the rest ride. You decide how much to save or put toward debt, automate that amount on payday, then spend what’s left guilt-free.

- Step 1: Pick your savings numbers (emergency fund, retirement, one short-term goal).

- Step 2: Automate transfers on payday.

- Step 3: Use one checking account for everything else. Track the balance weekly.

It’s not perfect, but it gets results. Think of it as “dieting by eating your salad first.” Boring? Maybe. Effective? Absolutely.

Who Should Use This

Use this if you want results with minimal effort, especially if you already spend conservatively. If your “fun money” tends to explode, pair this with weekly spending limits.

The Cash Envelope (or Digital Envelope) Method

Old-school but still deadly effective. You set spending limits for categories like groceries, dining, and fun, and you put the budgeted amounts into envelopes—actual cash or digital versions with separate accounts or app categories.

- Why it works: You feel the limit. When the envelope runs out, you stop.

- Great for: People who overspend in specific areas (looking at you, DoorDash).

Digital Envelope Hacks

If you hate cash, use:

- Bank sub-accounts with nicknames (Groceries, Fun, Gas).

- Prepaid cards for certain categories (travel, gifts).

- Budget apps that mimic envelopes (YNAB, Goodbudget, Monarch).

The 60/20/20 Rule (for Fluctuating Income)

If your income changes each month, lock in a percentage-based plan. Aim to live on 60% of your average income, then put 20% to savings and 20% to taxes or extra debt (adjust for your situation).

Set a “Base Budget”

Build your essentials on your lowest typical income month. During higher-income months, push extra toward savings, taxes, and a “future expenses” fund. This keeps you steady when the slow season hits.

Pick Your Method: A Simple Decision Guide

Can’t decide? Try this quick matchmaker:

- “I want easy.” Go 50/30/20 or Pay Yourself First.

- “I overspend a lot.” Use Cash/Digital Envelopes.

- “I want maximum control.” Zero-Based Budgeting.

- “My income is chaotic.” Percentage-based (60/20/20) with a base budget.

No method works if you ghost it. Check in weekly for 10 minutes. Adjust. Move on. Money likes attention, not obsession.

Make Your Budget Stick (Without Hating Life)

You don’t need monk-level discipline, but you do need systems. Here’s how to keep it painless:

- Automate everything: Bills, savings, debt payments—put them on autopilot.

- Use a “Buffer” category: $50-$150 for small surprises. Saves your sanity.

- Try a No-Spend weekday: Pick one day for zero discretionary spending. Weirdly powerful.

- Track with what you’ll actually use: Spreadsheet, app, or sticky notes. Fancy doesn’t equal effective.

- Review once a week: 10-minute Friday check-in: what’s left, what’s next, any fires?

Common Budgeting Traps to Avoid

- Being too strict: If you hate your budget, you’ll quit. Leave breathing room.

- Forgetting annual/irregular costs: Car registration, gifts, vet visits. Create a sinking fund.

- Chasing perfection: You’ll mess up sometimes. Adjust and keep going. IMO, consistency beats precision.

Tools That Actually Help

Use tools that match your style. Don’t marry an app because TikTok said so.

- For zero-based: YNAB (great for envelopes and goals), EveryDollar.

- For simplicity: Monarch, Simplifi, or a Google Sheet.

- For automation lovers: Banks with sub-accounts and automatic rules (Ally, Capital One, Revolut).

- For cash envelope fans: Digital envelopes or separate debit cards for categories.

FAQ

How do I budget if I live paycheck to paycheck?

Start tiny. Cover essentials first, then move $20-$50 per check into a starter emergency fund. Use envelopes for your worst spending category. As the emergency fund hits $500, shift a bit more to debt or savings. Momentum matters more than size at the start.

What if my expenses change a lot each month?

Use a base budget for essentials and percentage-based allocations for the rest. Create sinking funds for irregular costs like car maintenance or holidays. During higher-income months, pad those funds so low months don’t wreck you.

Should I pay off debt or save first?

Do both—but in order. Build a small emergency fund ($500–$1,500), then attack high-interest debt hard. Keep contributing a little to savings so you don’t backslide when life gets spicy. After debt, ramp up savings and investing.

How often should I change my budget?

Adjust monthly, check weekly. Your first month is a test; month two gets better; by month three, you’re dialed in. If you change jobs, move, or add a new bill, rework your numbers immediately.

Do I need budgeting apps to succeed?

Nope. Apps help, but pen and paper works if you actually use it. The best tool is the one you’ll check. If you love automation, apps shine. If you love control, spreadsheets win.

What’s a “sinking fund” and why does everyone rave about it?

It’s a mini-savings bucket for predictable-but-irregular expenses—car repairs, holidays, annual subscriptions. You stash a small amount each month so the bill doesn’t body-slam your budget later. Future-you will send thank-you notes.

Conclusion

Budgeting isn’t punishment—it’s a plan for your money to do what you want. Start simple, pick one method, and automate the boring stuff. You’ll make mistakes, you’ll adjust, and you’ll get better fast. Give it 90 days, and your bank account will look way less chaotic—promise.