How to Budget Without Feeling Restricted and Smile Again

Introduction

Kick the guilt off your budgeting, stat. You don’t have to live on ramen and restraint to get your money under control. Budgeting can feel friendly, flexible, even fun—if you do it right. Here’s a no-shriek, all-aboard-your-own-boat guide to budgeting without feeling restricted.

1) Start with a Reality Check, Not a Rulebook

Budgeting starts with honest numbers, not a sermon. Do you actually know where your money goes? Probably not, unless you’ve been abruptly staring at your bank app every Sunday. Here’s a simple truth: you can budget without micro-managing your life.

– List your essential expenses first: rent or mortgage, utilities, groceries, transportation. This is your safety net.

– Add a “fun fund” so you don’t twist into a budget zombie. You deserve treats, not torment.

– Track for a month, then trim. Not everything needs to be perfect, just practical.

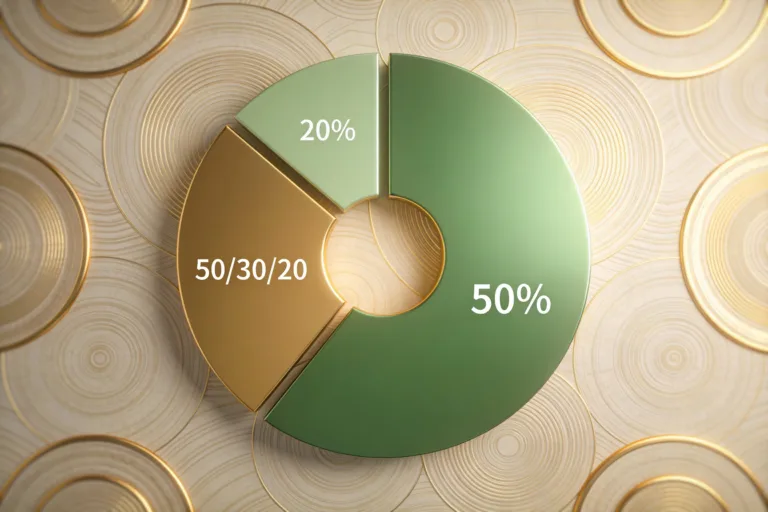

Subsection: The 50/30/20-ish Rule, Made Friendlier

If you’ve heard of 50/30/20, great. If not, here’s a chill version: 50% needs, 30% wants, 20% savings. It’s a guideline, not a law. If you’re in a high-cost area, you might push wants down to 25% and keep needs near 60%. The key: keep it simple, keep it sane.

2) Build a Budget That Bites Back, Nicely

A budget should protect your life, not imprison it. Focus on what actually matters to you. What do you value? Food, adventures, family time, wellness? Put those front and center.

– Create broad categories: Essentials, Habits, Joy, Future.

– Name the exact amount you’ll allocate to each, then live within those lines.

– Use a buffer. A little cushion helps you avoid the guilt-trap when something pops up.

Subsection: The “No-Guilt” Cushion

Give yourself a 5–10% wiggle room per category. If you overspend in one area, you don’t automatically get crushed elsewhere. You adapt. FYI, this is where the magic happens: you gain confidence because you know you can handle surprises.

3) Automate the Boring Stuff, Not the Fun Stuff

Automation is your friend. It makes saving invisible and bills painless. But you don’t want a robotic life; you want control with ease.

– Automate savings: set up transfers to a high-yield account the day after you get paid.

– Automate bills: avoid late fees by paying on or before due dates.

– Leave a little room for manual tweaks: sometimes you want to treat yourself; that’s not cheating, that’s living.

Subsection: The Plate-Share Trick

Treat your budget like a dinner plate: one big section for needs, a slightly smaller one for wants, and a tiny corner for plays. If you’re tempted to go overboard on a hobby, ask yourself: “Do I want this more than I want to sleep well this month?” If the answer is yes, adjust elsewhere, not in a frenzy.

4) Make Room for Treats Without Regret

Budgeting isn’t a constraint appendectomy; it’s a personalized plan that includes joy. Without joy, budgets collapse into rebellion. So, plan for pleasure.

– Set a monthly “fun fund.” This is where you chase experiences, not things.

– Batch-lunch days, not ban-lunch days. You’ll save money and avoid the “hangry wallet.”

– Plan micro-treats. A coffee shop splurge or a streaming night can be budget-friendly boosts.

Subsection: Tiny Treats That Save You Big

Small rewards create positive reinforcement. A $5 movie night or a $3 fancy latte can be the difference between sticking to your plan or falling off the wagon. IMO, celebrate small wins often.

5) Change the Script: From Scarcity to Strategy

Scarcity vibes sabotage budgets. Replace them with strategy vibes. When you feel restricted, you’ll resist. When you feel in control, you’ll commit.

– Reframe “budget” as “life plan.” It sounds friendlier and more accurate.

– Use positive language: “I choose to save this month” instead of “I can’t spend this.”

– Celebrate progress, not perfection. Tiny improvements compound into big wins.

Subsection: The Mindset Makeover Checklist

– Do you know where your money goes? Yes? Great. No? Track for a week.

– Can you cover essentials without stress? If yes, you’re already ahead.

– Are you saving something every month? If not, set a tiny automatic target to start.

6) Learn Your Personal Budget Rhythm

Everyone has a rhythm. Some people thrive on weekly check-ins; others prefer monthly. Find yours, then lean into it.

– Weekly quick-touches: a 10-minute review to adjust obvious drags.

– Monthly deep dive: assess saving progress and big bets (like paying down debt or saving for a trip).

– Seasonal reframing: holidays, birthdays, vacations require extra planning.

Subsection: The Five-Minute Budget Reset

Set a timer for five minutes, check last week’s spend, adjust the next seven days, and call it a day. If you’re done in five, you’re done. Short bursts beat marathon guilt.

7) Use Tools That Speak Your Language

Apps and spreadsheets can make budgeting feel empowering, not punishment. Pick tools that match your vibe—no judgment, just clarity.

– Simple trackers: apps that categorize automatically and show trends.

– Visuals: charts and graphs that reveal patterns without requiring a PhD in accounting.

– Sync across devices: so you can peek at your budget while ordering takeout, not after you’ve spent the money.

Subsection: The Minimalist Toolkit

If you’re overwhelmed by options, start basic:

– One income, one savings account, one checking account

– One budget template (either digital or a simple notebook)

– One monthly review ritual

You’ll be surprised how much you can accomplish with a clean setup.

8) Practical Scenarios: Quick Wins You Can Use Today

Real-life tweaks beat theory any day. Here are some quick wins that don’t require a social media guru level of discipline.

– Rethink recurring subscriptions: keep what you actually use; cancel the rest.

– Groceries with a twist: plan meals, shop with a list, and buy generic when sensible.

– Commute smarter: carpool, public transit, or biking to save serious money over time.

– Debt daisy chain: if you have high-interest debt, tackle it with a focused payoff plan, but don’t neglect your emergency cushion.

9) FAQ

How do I budget if I’m living paycheck to paycheck?

Start with a tiny emergency fund, even if it takes a while. Then automate whatever you can—savings, bills, and a small buffer. Track overspending days and plan for the next one. It’s about momentum, not perfection.

Is it okay to tweak my budget mid-month?

Absolutely. Budgets aren’t tattoos; they’re living documents. If you realize you overspent on groceries but underspent on dating, adjust what you’ll cut or move forward. Flexibility beats guilt, every time.

What if I have irregular income?

Treat the average monthly income as your baseline. Build a buffer for the months when money is lean, and use the good months to pad savings or debt payoff. It’s all about smoothing the ride.

How do I stay motivated to save without feeling deprived?

Attach savings to goals you care about—vacations, buying a home, freedom from debt. Tie small wins to those goals and celebrate them. FYI, tiny wins add up faster than you think.

Should I use cash or cards?

Cards are convenient and trackable; cash adds a tactile reminder of the money leaving your pocket. A hybrid approach often works: use a debit card for most items and keep a cash envelope for discretionary spends like coffee or snacks.

Conclusion

Budgeting doesn’t have to feel like a prison sentence. It can be a practical, even enjoyable, way to steer your life toward what matters. Start with honest numbers, automate the boring stuff, and keep room for joy. You’ll gain control without losing spontaneity. IMO, the secret is to treat your money like a trusted ally, not a fearsome overlord. Ready to try a friendlier budgeting approach and see how it changes your month? Let’s do it together.