Best Budget Planners for Low Income

Let me guess—you’re trying to manage your money, but every “budget planner” you find assumes you have spare cash just chilling in your checking account. Yeah… same. 😅

When money feels tight, you don’t need a fancy spreadsheet screaming “JUST EARN MORE.” You need something simple, realistic, and actually usable on a low income.

I’ve tested planners when my budget was very much in survival mode, and trust me—not all planners work when every dollar already has a job. Let’s talk honestly about the best budget planners for low income, what actually helps, and what you can safely ignore without guilt.

Why Most Budget Planners Fail on a Low Income

Before we talk about what works, let’s call out what doesn’t.

Most planners assume:

- You can save $500 a month (LOL).

- Your income stays the same every month.

- Emergencies politely wait for payday.

Sound familiar? Yeah, didn’t think so.

When money feels tight, a planner must help you prioritize survival first, not shame you for skipping a “fun money” category. IMO, that mindset shift matters more than the planner itself.

What a Budget Planner for Low Income Must Do

Keep Things Simple (Like, Really Simple)

Complex budgets drain mental energy fast. When money already stresses you out, extra columns just make it worse.

A good budget planners low income option should:

- Track needs first (rent, food, utilities)

- Let you ignore perfection

- Feel flexible instead of rigid

Ever opened a planner and instantly felt tired? That’s your cue to close it.

Focus on Cash Flow, Not Fantasy Savings

Low income budgeting works best when you track:

- What comes in

- What must go out

- What’s left (even if it’s $17)

That $17 still matters. Why? Because awareness beats avoidance every time.

Best Budget Planner Types for Low Income (What Actually Works)

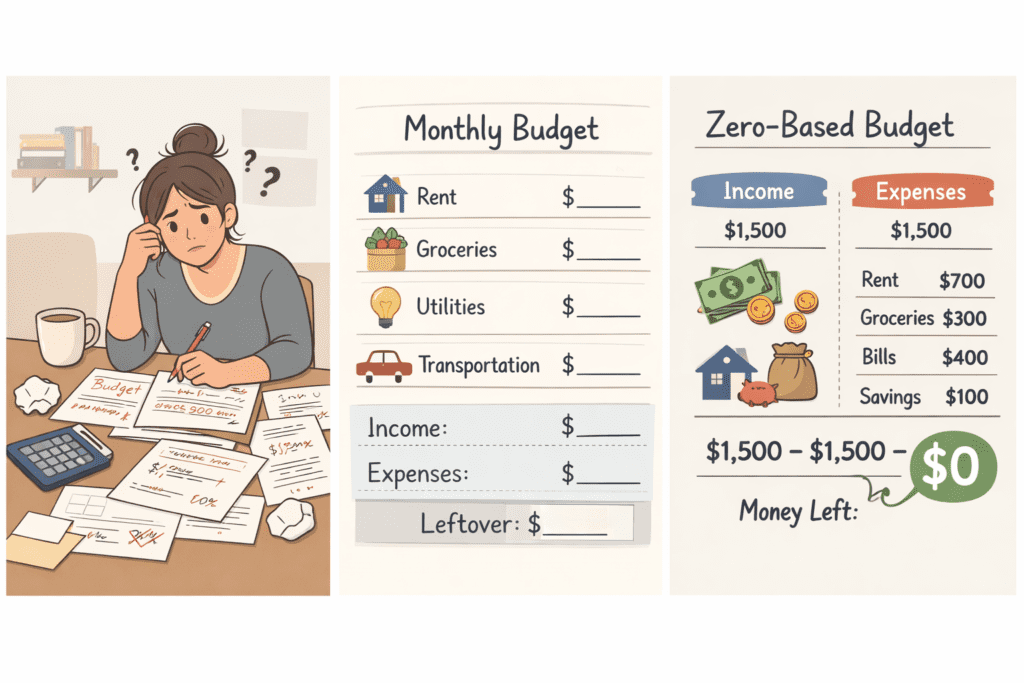

1. Zero-Based Budget Planners (My Personal Favorite)

I swear by this one. When money runs tight, zero-based budgeting gives every dollar a purpose.

Here’s how it works:

- Income minus expenses equals zero

- You assign every dollar, even small ones

- Nothing feels “lost”

Why it works on low income:

- You stay intentional

- You avoid accidental overspending

- You feel oddly powerful telling money where to go

FYI, zero doesn’t mean you spend everything—it means you decide everything.

2. Printable Budget Planners (Free & No Pressure)

Printables saved me when apps felt overwhelming.

Why printable planners rock for low income:

- They cost $0 (huge win)

- You control how detailed things get

- You can ignore pages that don’t apply

Look for printables with:

- One-page monthly overview

- Simple expense tracking

- No investment sections (you’re budgeting, not daydreaming)

Pro tip: Print just the pages you’ll actually use. No gold stars for unused sheets.

3. Weekly Budget Planners (Because Monthly Feels Too Big)

Ever tried planning an entire month on a low income and felt instant anxiety? Same.

Weekly planners help because:

- You focus on short-term survival

- You adjust faster when things go sideways

- You avoid that “I already blew it” feeling

I used weekly budgeting during unpredictable income months, and honestly? It kept me sane.

Best Free Budget Planners for Low Income (Seriously Free)

Let’s talk free stuff that actually works—no hidden upsells, no guilt trips.

1. One-Page Budget Worksheets

These focus on:

- Income

- Fixed expenses

- Variable expenses

That’s it. No fluff.

Why they work:

- You finish them in 10 minutes

- You see reality fast

- You feel less overwhelmed

Simple beats fancy every time.

2. Expense-Only Trackers (Underrated but Powerful)

Sometimes, you don’t need a full planner. You just need to know where money leaks.

Expense trackers help you:

- Spot small spending patterns

- Reduce guilt-based spending

- Make smarter swaps

Ever wonder why money disappears so fast? This answers that question real quick.

Digital vs Paper Budget Planners: Which Is Better?

Short answer? Whatever you’ll actually use.

Longer answer:

Paper Planners Work Best If You:

- Like writing things down

- Feel overwhelmed by apps

- Want a slower, intentional process

Paper budgeting helped me feel connected to my money when things felt chaotic.

Digital Planners Work Best If You:

- Get paid irregularly

- Need quick edits

- Track spending on the go

Just avoid apps that push premium upgrades every five minutes. That’s not helpful :/

Budget Categories That Make Sense on a Low Income

Here’s a realistic setup that won’t insult your intelligence.

Start with:

- Housing

- Utilities

- Food

- Transportation

Then add (if possible):

- Minimum debt payments

- Small emergency buffer (even $10 counts)

Skip categories like:

- “Luxury”

- “Investments”

- “Travel goals”

You can add those later. Right now, stability wins.

Common Budgeting Mistakes (I Made These, So You Don’t Have To)

Expecting Perfection

Missed a week? Overspent on groceries? Congrats—you’re human.

Budgeting works when you:

- Adjust

- Continue

- Stop punishing yourself

Consistency beats perfection. Always.

Ignoring Small Wins

Saved $20? Paid a bill on time? Didn’t overdraft?

That counts. Celebrate it.

Low income budgeting improves mindset first, numbers second.

How to Stick With a Budget When Money Feels Tight

Make It Short-Term

Don’t plan six months ahead. Plan:

- This week

- Next paycheck

- One bill at a time

Short horizons reduce stress.

Review Weekly, Not Daily

Daily tracking burns people out fast.

Weekly check-ins:

- Keep you aware

- Feel manageable

- Help you adjust calmly

Ask yourself: What worked this week? What didn’t?

Final Thoughts: The Best Budget Planner Is the One You’ll Use

Here’s the truth nobody tells you:

The best budget planners for low income aren’t fancy. They’re forgiving.

They:

- Meet you where you are

- Respect your reality

- Help you feel more in control

If your planner makes you feel worse about money, ditch it. Budgeting should reduce stress, not add to it.

Start small. Stay consistent. And remember—you’re doing the best you can with what you have, and that already counts more than you think 🙂