Best Way to Pay Off Debt Step by Step

Let me guess—you’re tired of debt sitting in the background of your life like that annoying app notification you keep ignoring 📱. I’ve been there. I remember checking my bank app, sighing dramatically, and promising myself I’d “start next month.” Sound familiar?

Here’s the good news: the best way to pay off debt doesn’t require magic, a massive salary, or monk-level discipline. You just need a clear plan, a little consistency, and a mindset shift that actually sticks. Let’s walk through this together, step by step, like two friends figuring it out over coffee ☕.

Step 1: Face the Numbers (Yes, All of Them)

I know, I know—this part feels about as fun as cleaning your email inbox from 2016. But trust me, clarity beats anxiety every single time.

List Every Single Debt

Grab a notebook or spreadsheet and write down:

- Who you owe

- Total balance

- Interest rate

- Minimum payment

No skipping the “small” ones. Small debts love attention, IMO 😅.

Why This Step Works

When I first did this, I felt instant relief. Seeing everything in one place made the problem feel finite, not endless. Ever noticed how vague money stress feels heavier than real numbers?

Bold truth: You can’t fix what you refuse to see.

Step 2: Stop Adding New Debt (Temporary Pain, Long-Term Gain)

This step doesn’t get enough hype, but it matters a lot.

Pause the Damage

You don’t need to cut up your credit cards dramatically (unless that motivates you). Just:

- Leave cards at home

- Remove saved cards from apps

- Switch to cash or debit for daily spending

Why This Step Matters

Paying off debt while creating new debt feels like bailing water out of a sinking boat with a spoon. Ever tried that? Yeah…not great.

Key takeaway: You don’t need perfection—just a pause.

Step 3: Build a Tiny Emergency Fund (Before Going Hard on Debt)

Wait—save money before paying off debt? Yep. Stay with me.

Aim for ₹10,000–₹25,000 (or $500–$1,000)

This small buffer protects you from:

- Unexpected repairs

- Medical bills

- “Oops” life moments

Why This Actually Speeds Things Up

Before I had an emergency fund, every surprise expense sent me straight back to my credit card. That cycle felt brutal. Once I built a buffer, I stopped backsliding.

Bold reminder: An emergency fund keeps debt from sneaking back in through the side door.

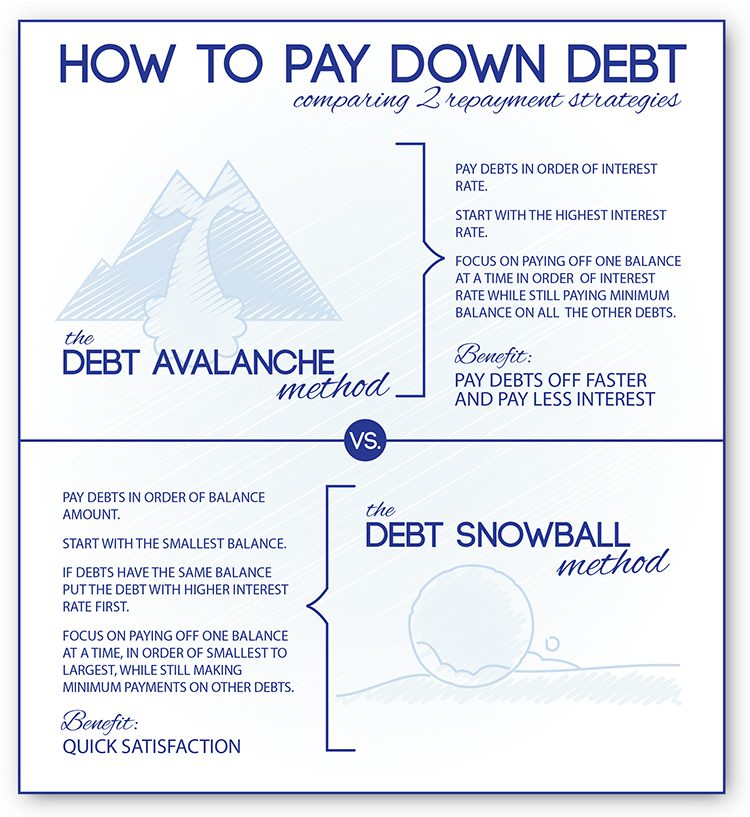

Step 4: Choose Your Debt Payoff Method (Snowball vs Avalanche)

Here’s where strategy kicks in. And yes, people love arguing about this one 😄.

Option 1: Debt Snowball

You pay off debts from smallest to largest balance, ignoring interest rates at first.

Why people love it:

- Quick wins

- Motivation skyrockets

- Momentum feels addictive

Option 2: Debt Avalanche

You focus on debts with the highest interest rate first.

Why it works:

- You save more money long-term

- Interest stops bleeding your wallet

Which Is the Best Way to Pay Off Debt?

Honestly? The method you’ll stick with. I started with snowball because I needed emotional wins. Math didn’t motivate me—progress did. Ever felt that rush after checking something off a list?

FYI: Both methods work. Consistency matters more than perfection.

Step 5: Find Extra Money Without Feeling Miserable

You don’t need a second job that steals your soul. You just need small wins.

Quick Ways to Free Up Cash

- Cancel unused subscriptions (yes, even that one :/)

- Negotiate bills like internet or phone

- Sell stuff you don’t use anymore

- Redirect bonuses or refunds to debt

My Personal Rule

If I didn’t miss the money before, I won’t miss it now. That mindset helped me throw extra cash at debt without resentment.

Bold truth: You don’t need more income—you need intention.

Step 6: Automate Minimum Payments (Then Add Extra Manually)

Automation keeps you consistent when motivation dips.

How to Do It Right

- Automate minimum payments for all debts

- Manually add extra money to your target debt

This combo prevents missed payments while letting you stay flexible.

Why This Reduces Stress

I stopped worrying about due dates the moment I automated. Fewer mental tabs open = more peace. Who doesn’t want that?

Key benefit: Automation protects progress even on bad days.

Step 7: Track Progress Like a Slightly Obsessed Human

Tracking progress feels oddly satisfying. Don’t fight it—embrace it.

Simple Tracking Ideas

- Color in a debt thermometer

- Use a spreadsheet

- Write balances monthly in a notebook

Why This Keeps You Going

Watching balances drop reminds you that effort works. Every update tells your brain, “Hey, this isn’t pointless.”

Bold reminder: Progress fuels motivation—not the other way around.

Step 8: Adjust Your Budget Without Hating Your Life

Budgets get a bad rep, but they don’t need to feel restrictive.

Keep It Real

Your budget should include:

- Fun money (yes, seriously)

- Realistic food spending

- Guilt-free rest days

When I tried extreme budgeting, I quit fast. When I allowed flexibility, I stayed consistent.

Rhetorical check: Would you rather move slowly or quit entirely?

Step 9: Use Windfalls Wisely (But Don’t Be a Robot)

Tax refunds, bonuses, gifts—they help a lot.

My Favorite Rule

Use 70–80% for debt, and enjoy the rest. Balance matters.

This approach kept me sane while still making serious progress.

Bold takeaway: You can be responsible and human 🙂

Step 10: Prepare for Life After Debt (Yes, It Exists)

Debt payoff isn’t the finish line—it’s the launchpad.

What Comes Next

- Build a bigger emergency fund

- Start investing

- Set long-term money goals

Thinking ahead kept me motivated during the final stretch. Ever noticed how clear the future feels when debt stops blocking the view?

Key mindset shift: Paying off debt creates options, not restrictions.

Common Mistakes That Slow Everything Down

Let’s save you some frustration.

Avoid These Traps

- Trying to be “perfect”

- Comparing your journey to others

- Ignoring burnout signs

- Quitting after one bad month

I messed up plenty of times. I still finished strong. You can too.

Bold reminder: Consistency beats intensity every time.

Why This Really Is the Best Way to Pay Off Debt

This step-by-step approach works because it:

- Builds confidence early

- Protects you from setbacks

- Adapts to real life

- Keeps motivation alive

Debt payoff isn’t just math—it’s emotional. When your plan respects that, results follow.

Final Thoughts: You’ve Got This (Seriously)

If debt feels overwhelming right now, take a breath. You don’t need to do everything today. You just need to start with one step.

Write the list. Build the buffer. Pick a method. Repeat tomorrow.

I’ve walked this road, stumbled plenty, and still crossed the finish line 🎯. And if I can do it, you absolutely can.

So…what’s your first step going to be?