How to Stop Self Sabotaging Your Finances Without the Drama

I know the feeling: you tell yourself you’ll sort out your finances this month, and somehow you end up buying oddly specific coffee gadgets you didn’t need. Self-sabotage is loud, sneaky, and incredibly convincing. Let’s cut through the noise and get you back in control—without turning budgeting into a full-blown horror movie.

Why you might be sabotaging your own wallet (and not even realizing it)

You wake up with good intentions, then the day takes a nosedive into impulse town. It happens because your brain loves dopamine, not budgets.

– You crave instant gratification, especially when money is involved.

– You’ve built habits that work against long-term goals, like payday shopping sprees or “just this once” splurges.

– You’re avoiding bigger issues, like debt or a lack of emergency savings, by throwing money at shiny objects.

What you’re really fighting is a tug-of-war between your short-term wants and your long-term values. If you want to win, you need a plan that respects both sides of the coin.

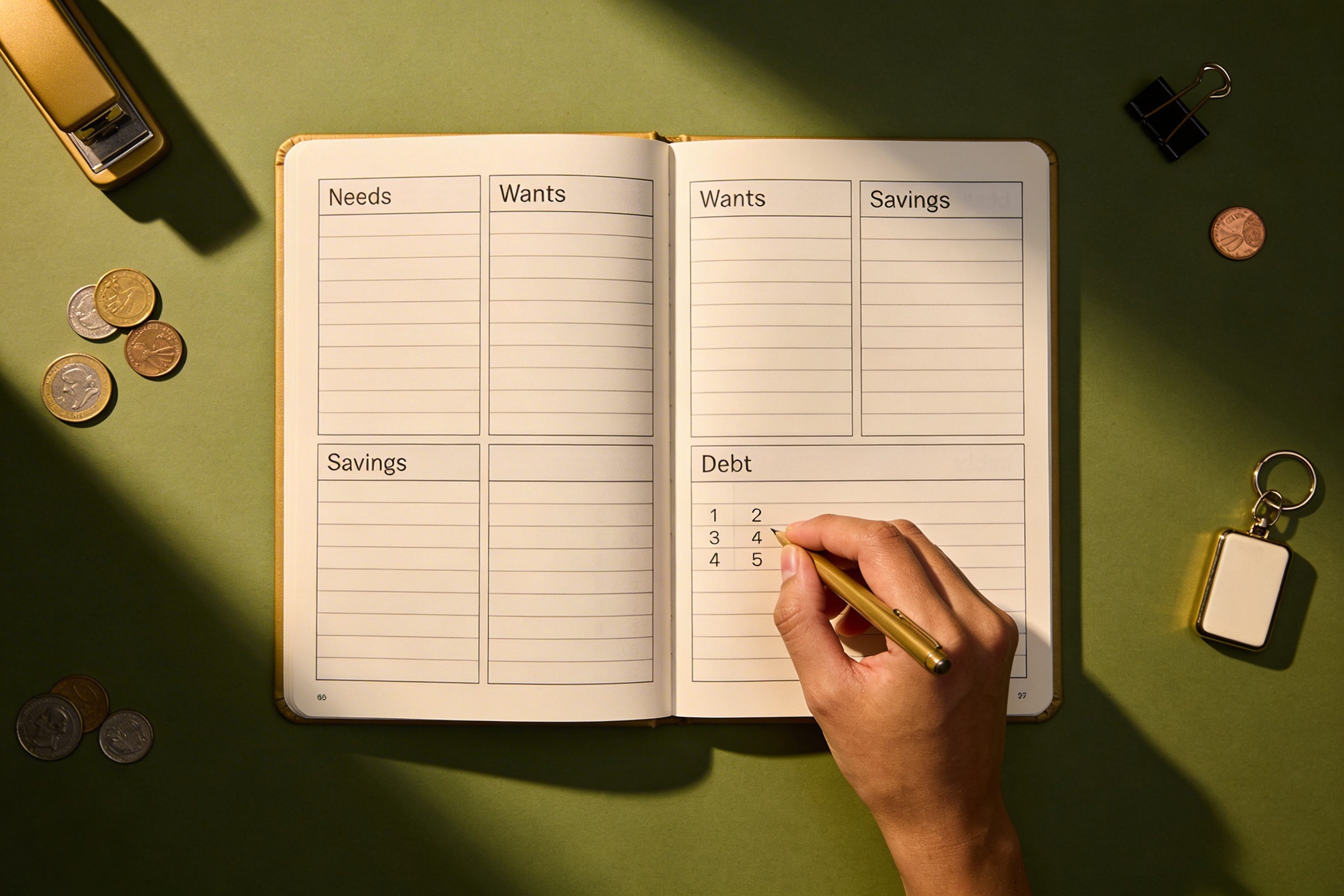

Get your core numbers straight (no shame, just clarity)

Let’s start with the boring-but-powerful stuff. If you don’t know where your money actually goes, you’re doomed to repeat the same mistakes.

- Track for 30 days. No excuses. Your future self will thank you.

- Categorize spending into needs, wants, and savings/debt payments.

- Identify the leaks: recurring subscriptions you forgot, impulse buys, and weekly takeout binges.

- Cut the fat by canceling unused subscriptions. It’s amazing how much you’ll save without feeling deprived.

- Automate essential savings first. If you never see it, you won’t miss it.

- Set a realistic budget that allows room for a weekly treat. Yes, you can have dessert and still hit goals.

Build a silly-simple plan you actually enjoy

If your plan feels like a math test, you’ll bail. Make it approachable and human.

- Create a “must-do, nice-to-do, would-like-to-do” list for each category: housing, food, transport, fun, and future.

- Assign a monthly target to each category, but keep the numbers flexible enough to absorb life’s curveballs.

- Use micro-goals like “$5 daily transfer to savings” rather than one giant, scary goal.

Subsection: The 80/20 rule in action

If 20% of your expenses are driving 80% of the risk, you’ll want to tackle those first.

– Identify that one big recurring cost that irritates you every month.

– Negotiate or switch to cheaper options without ruining your life.

Confront the sneaky saboteurs (and boss them back into line)

Sabotage wears many disguises. Here’s how to spot and stop them.

- Emotional spending—sudden splurges after a bad day. Break the cycle with a 24-hour rule or a cooling-off period.

- Shopping as therapy—don’t treat a mood with a cart. Try a walk, a chat with a friend, or a quick workout first.

- Debt-avoidance denial—thinking “I’ll deal with it later” only makes later bigger and scarier.

Subsection: Routine wins that reduce friction

Small changes compound.

- Turn on autopay for essentials to avoid late fees and stress.

- Set up a weekly money date with yourself. Treat it like a friendly check-in, not a courtroom appearance.

- Use a spending limit on category apps—color-coded alerts keep you honest.

Automation that actually feels personal

Automation isn’t about turning you into a robot; it’s about clearing brain space for important decisions.

- Savings first: automatic transfers on payday, even if it’s small.

- Bills paid on autopilot with a single dashboard view so you know what’s due without opening a dozen apps.

- Emergency fund target: aim for 3–6 months of expenses. Start with a modest goal and build momentum.

Subsection: Why tiny savings actually matter

Tiny saves add up. Think of it as emotional armor against surprise expenses. FYI, consistency beats intensity here.

Reframe money as a tool, not a stressor

If money feels like a villain, you’ll treat it like one. Change the script.

- Link money to values. If you value freedom, tie savings to trips or gigs you’re excited about.

- Celebrate wins, no matter how small. A small victory deserves a mini-cheer, not a guilt trip.

- Replace guilt with curiosity. Ask yourself: what pattern led to this spend, and how can I adjust?

When to seek help (and when you probably don’t need a guru)

Sometimes you need backup, not a magic wand.

- Big, persistent debt or spending that feels out of control: consider a financial coach or credit counselor.

- Learning style matters. If you can’t self-regulate, a structured course or accountability partner helps a lot.

- DIY is fine, but don’t ignore serious red flags like aggressive interest rates or predatory terms.

Practical tools to keep you honest

Here are some friendly, no-judgment tools that actually work.

- Budgeting apps with visual progress—go for ones that show you trends, not just numbers.

- Cash envelope or digital envelope system to limit overspending in tricky categories.

- Automatic debt snowball/avalanche to gain momentum on payoff without feeling overwhelmed.

Frequently asked questions

How do I stop impulse buying without feeling deprived?

Answer: Make space for small pleasures on a schedule, not a shopping spree. Set a weekly “fun budget” you can actually use. If you still crave something, wait 24 hours and ask yourself if you’ll still want it tomorrow. Usually you won’t.

What’s the fastest way to build an emergency fund?

Answer: Start with a tiny, automatic weekly transfer. Even $5 or $10 adds up fast. Celebrate when you hit milestones, and keep the fund separate so you don’t dip into it for non-emergencies.

Is budgeting really necessary if I’m not broke?

Answer: Yes. Budgeting isn’t about deprivation; it’s about choice. It helps you align your spending with your values and life goals, and it reduces anxiety around money.

How do I convince my friends I’m not a buzzkill for saying no to dinner out every week?

Answer: Frame it as a shared goal, not a restriction. Propose cheaper alternatives, or suggest you cover the cheaper items and put the rest toward a bigger goal. FYI, friends respect honesty.

What if I mess up again next month?

Answer: It happens. The key is to reset quickly. Reassess what tripped you up, adjust your plan, and move forward. Consistency beats perfection any day.

Conclusion

You can stop sabotaging your finances without turning life into a grind. Start with a clear picture of where your money goes, short, friendly goals, and a little automation that does the heavy lifting. Remember, you’re not aiming for perfection—just steady progress. So take a breath, pick one easy win today, and watch momentum build. You’ve got this.