50/30/20 Budget Rule Explained (Simple Beginner Guide)

Ever feel like your money disappears faster than free pizza at a party? You’re not alone. Budgeting sounds about as fun as watching paint dry, but the 50/30/20 rule is the lazy person’s cheat code to financial sanity. No spreadsheets, no headaches—just three simple buckets for your cash. Let’s break it down.

What the Heck Is the 50/30/20 Budget Rule?

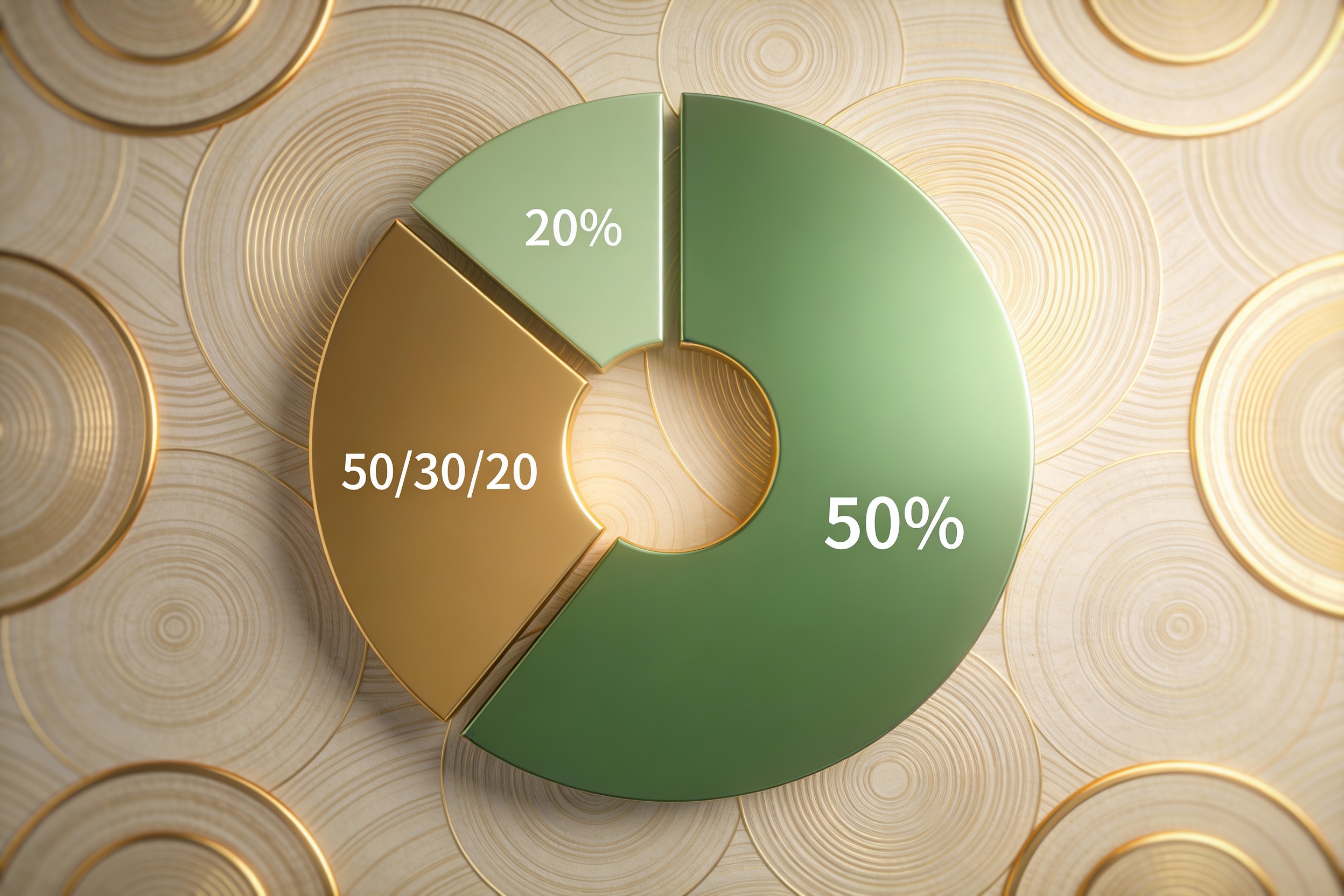

Created by Senator Elizabeth Warren (yes, *that* Elizabeth Warren) in her book *All Your Worth*, the 50/30/20 rule is basically a money pie sliced into three easy pieces:

- 50% Needs: Rent, groceries, insurance—the “you’ll cry if you don’t pay these” stuff.

- 30% Wants: Netflix, avocado toast, that impulse-buy candle that smells like “ocean breeze” but honestly just smells like wax.

- 20% Savings/Debt: Future-you’s safety net or digging out of past-you’s bad decisions.

The beauty? It’s flexible. Unlike diets that ban carbs or budgets that demand you live on rice and beans, this one lets you breathe.

Why the 50/30/20 Rule Works for Beginners

Most budgets fail because they’re *way* too strict. The 50/30/20 rule wins because:

- It’s stupid simple. Math haters, rejoice—you only need to divide your paycheck three ways.

- Guilt-free spending exists. That 30% “wants” bucket means you can still enjoy life without feeling like a financial failure.

- It scales with you. Whether you make $30K or $300K, the percentages stay the same.

FYI, this isn’t a magic wand—it won’t fix a $5K monthly shopping habit. But it *will* give you a reality check without the soul-crushing austerity of other budgets.

How to Actually Apply the 50/30/20 Rule

Step 1: Calculate Your After-Tax Income

This is the money that *actually* hits your bank account. If your paycheck is $4,000 a month after taxes and deductions, that’s your starting number. Pro tip: If you’re freelance or have side gigs, average your last 3-6 months of income—don’t rely on your best month ever.

Step 2: Slice That Income Like a Pizza

Using that $4,000 example:

- Needs (50%): $2,000 for rent, utilities, groceries, etc.

- Wants (30%): $1,200 for takeout, hobbies, and that gym membership you swear you’ll use.

- Savings/Debt (20%): $800 for emergency funds or paying off credit cards.

Step 3: Adjust If You’re Way Off

If your “needs” are eating up 70% of your income, you’ve got two options:

- Cut costs: Downsize your apartment, switch to generic brands, or negotiate bills.

- Boost income: Side hustles, asking for a raise, or selling stuff you don’t need (yes, even your collectible Funko Pops).

What Counts as a “Need” vs. a “Want”? (The Gray Area)

This is where people panic. Here’s the deal:

- Needs: Rent, basic groceries, health insurance, *minimum* debt payments, and transportation to work.

- Wants: Eating out, premium Spotify, designer clothes, and anything labeled “artisanal.”

The fuzzy middle? “Upgraded” things. A $40 phone plan is a need; a $120 plan with unlimited emojis is a want. IMO, if you’re arguing with yourself about it, it’s probably a want.

Common Mistakes (And How to Avoid Them)

Mistake #1: Ignoring Irregular Expenses

Car repairs, annual subscriptions, and holiday gifts don’t care that you forgot to budget for them. Divide yearly costs by 12 and stash that cash monthly.

Mistake #2: Treating Savings Like an Afterthought

Pay your future self *first*. Automate transfers to savings so you never “accidentally” spend that 20%.

Mistake #3: Being Too Rigid

Some months, you’ll overspend on wants or have a surprise need. That’s life. Adjust and move on—no self-flagellation required.

FAQ: Your Burning 50/30/20 Questions, Answered

1. Does student loan debt go in “needs” or “savings/debt”?

Minimum payments are a *need* (you gotta pay ‘em). Anything extra goes in the 20% bucket.

2. What if I can’t hit the 50% needs target?

You’re not alone—especially in high-cost areas. Do your best, but focus on increasing income long-term.

3. Can I save more than 20%?

Absolutely! If you’re crushing it, bump up savings and cut wants. Just don’t burn out.

4. Should I include retirement in the 20%?

Yep. Retirement savings count as savings. If your employer matches 401(k) contributions, that’s free money—take it.

Final Thoughts: Try It Before You Knock It

The 50/30/20 rule isn’t perfect, but it’s the easiest on-ramp to budgeting without losing your mind. Start tracking your spending for a month (apps like Mint help), then adjust the ratios if needed. Remember: The goal isn’t restriction—it’s control. Now go forth and spend that 30% on something ridiculous. You’ve earned it.